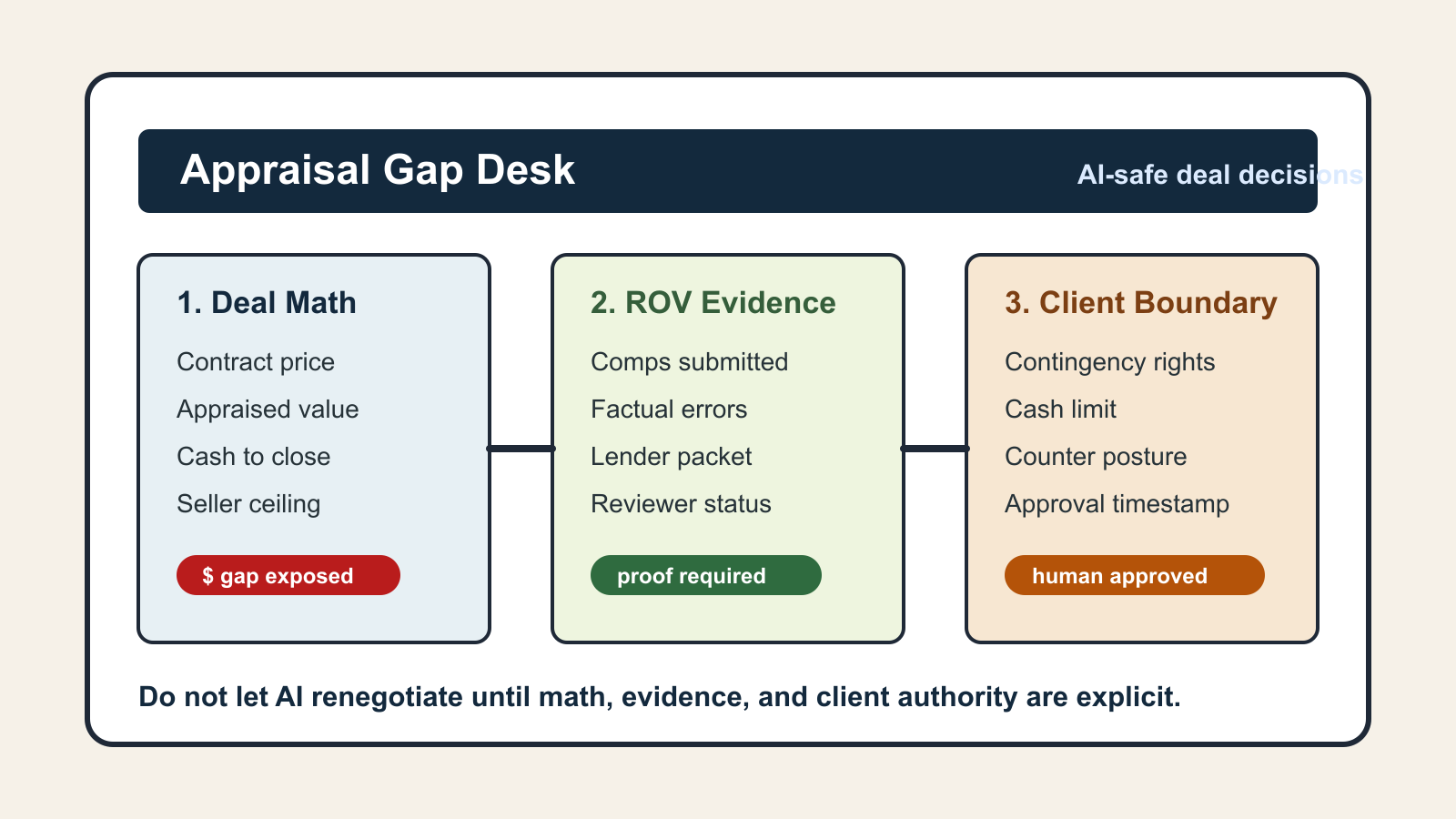

Build an Appraisal Gap Desk Before AI Renegotiates Deals

AI can already summarize comparable sales, draft buyer updates, and turn a low appraisal into polished renegotiation language. That is useful only after the team has decided what the appraisal means, which evidence is credible, what the contract allows, and who has authority to move money.

The missing operating layer is an appraisal gap desk. It is not another document folder. It is a structured decision surface for every deal where the appraised value, contract price, loan structure, contingency status, buyer cash, seller flexibility, and reconsideration-of-value evidence have to line up before anyone asks AI to write a recommendation.

Without that desk, AI will tend to make the problem sound simpler than it is: "ask for a price reduction," "cover the gap," or "request a reconsideration." In real transaction work, those choices affect earnest money risk, lender timing, seller proceeds, client trust, and closing probability.

Why this needs a dedicated queue

Current market data makes appraisal work a live operational issue. NAR's latest REALTORS Confidence Index reported that 7 percent of recent contracts were delayed because of appraisal issues. The same report showed that 19 percent of buyers waived the appraisal contingency, down from 23 percent one month earlier but still high enough to create real cash and risk questions when values miss.

The broader March market is not removing that pressure. NAR reported existing-home sales down 3.6 percent month over month, inventory at 4.1 months of supply, and a median existing-home price of $408,800, up 1.4 percent year over year. That mix creates local nuance: some buyers have more negotiating leverage, while constrained inventory and price growth can still produce low-appraisal conflicts on the exact homes people want.

Redfin's February 2026 appraisal-gap guide says roughly 8 percent of appraisals come in below contract price. Its April 2026 buyer-seller analysis also showed buyers holding more negotiating power in many large metros. The point for operators is not that every market is the same. It is that appraisal strategy has to combine local market leverage, lender rules, contract language, and client cash capacity before automation drafts anything.

What the desk should hold

Start with one row per appraisal event, not one row per transaction. A transaction can have an appraisal waiver, a clean appraisal, a low appraisal, a reconsideration request, a revised value, a price change, a credit change, or a fallout event. Each event needs state.

The minimum fields are:

- Contract price, appraised value, and dollar gap.

- Loan type, down payment, appraisal contingency status, and financing contingency deadline.

- Buyer cash available above planned closing costs.

- Seller concession ceiling, price-reduction floor, and net-proceeds sensitivity.

- Appraisal delivery date, response deadline, and expected lender turn time.

- Comparable sales submitted, comparable sales rejected, factual errors found, and missing property features.

- Reconsideration-of-value status, owner, evidence packet link, lender response, and final result.

- AI permission level: summarize evidence, draft client explanation, draft lender packet, draft seller counter, or escalate before writing.

The desk should also hold the client-approved decision boundary. That might be "buyer can cover up to $12,000," "seller will reduce price by no more than $8,000," or "do not submit an ROV unless the lender confirms these three comps are acceptable." AI should see those boundaries before it writes.

Separate three problems

Most appraisal-gap confusion comes from mixing three different problems.

The first is the math problem. How large is the gap, how does it change cash to close, what happens to loan-to-value, and what combinations of price change, credit, cash, or loan adjustment are actually possible?

The second is the evidence problem. Is the appraisal low because of a factual error, a missing feature, weak comparable selection, timing, condition, concessions, or a legitimate market signal? FHFA defines reconsideration of value as a request for the appraiser to reassess value because of reporting deficiencies, comparable-selection issues, or additional information the appraiser should consider. That is an evidence workflow, not a complaint workflow.

The third is the negotiation problem. What does the contract allow, what leverage does each side have, what deadline is controlling the conversation, and what outcome best protects the client? A buyer with an appraisal contingency and spare cash is in a different posture than a buyer who waived the contingency and needs every dollar preserved for closing.

AI can help with each problem, but it should not blend them. Ask it to calculate scenarios from approved inputs, organize an evidence packet, or explain options in plain English. Do not ask it to decide the client posture from a PDF and a few CRM notes.

Make ROV evidence operational

Fannie Mae's borrower-initiated reconsideration-of-value guidance was updated in September 2025 and points lenders back to Selling Guide section B4-1.3-12 for comprehensive requirements. Its FAQ says lenders are responsible for making sure borrower ROV requests meet minimum requirements before sending them to the appraiser, and that the borrower may request a maximum of one ROV for each appraisal report.

That matters for real estate teams because weak ROV packets waste the one shot. The desk should require every ROV candidate to identify the exact issue: factual error, omitted feature, wrong property condition, missed concession adjustment, stronger comparable sale, or possible bias concern. Each item should have a source link, property address, sale date, adjustment rationale, and reviewer.

Use a simple packet status:

- Drafting means the team is gathering evidence.

- Ready for lender review means the packet has no unsupported comps or vague objections.

- Submitted means the lender has accepted the packet into its process.

- Accepted value change means the appraiser or lender outcome changed the deal math.

- No value change means negotiation has to continue without promising the client another review path.

This keeps AI from writing aggressive ROV language around weak evidence. The model can format and summarize, but the desk decides whether the evidence is usable.

CRM views that make this useful

Create saved views that expose risk before the deadline.

The first view is "low appraisal inside five days." It should show gap size, contingency status, financing deadline, buyer cash range, seller ceiling, and whether a client decision is missing.

The second view is "ROV evidence incomplete." It should show every proposed comparable, the factual issue it supports, who reviewed it, and whether the lender has confirmed packet requirements.

The third view is "AI drafted, human approval missing." Any appraisal-gap email, seller counter, buyer explanation, or lender packet drafted by AI should stay there until the responsible agent, broker, lender, or client approves it.

These views turn appraisal gaps into managed work instead of stressful inbox threads. They also make post-close review possible: which markets produced repeated gaps, which offer strategies caused cash exposure, which agents waived contingencies without a coverage plan, and which lenders processed ROVs cleanly.

The implementation rule

Do not let AI renegotiate from the appraisal report alone. First create the appraisal gap desk, separate math from evidence from negotiation posture, record the client boundary, and attach the ROV packet status. Then let AI summarize options, draft explanations, and prepare clean language inside those constraints.

The teams that benefit from AI in appraisal work will not be the ones with the fastest draft. They will be the ones that can prove the draft came from verified values, contract rights, lender-ready evidence, and a client-approved decision boundary.

Written by

Ben Laube

AI Implementation Strategist & Real Estate Tech Expert

Ben Laube helps real estate professionals and businesses harness the power of AI to scale operations, increase productivity, and build intelligent systems. With deep expertise in AI implementation, automation, and real estate technology, Ben delivers practical strategies that drive measurable results.

View full profile