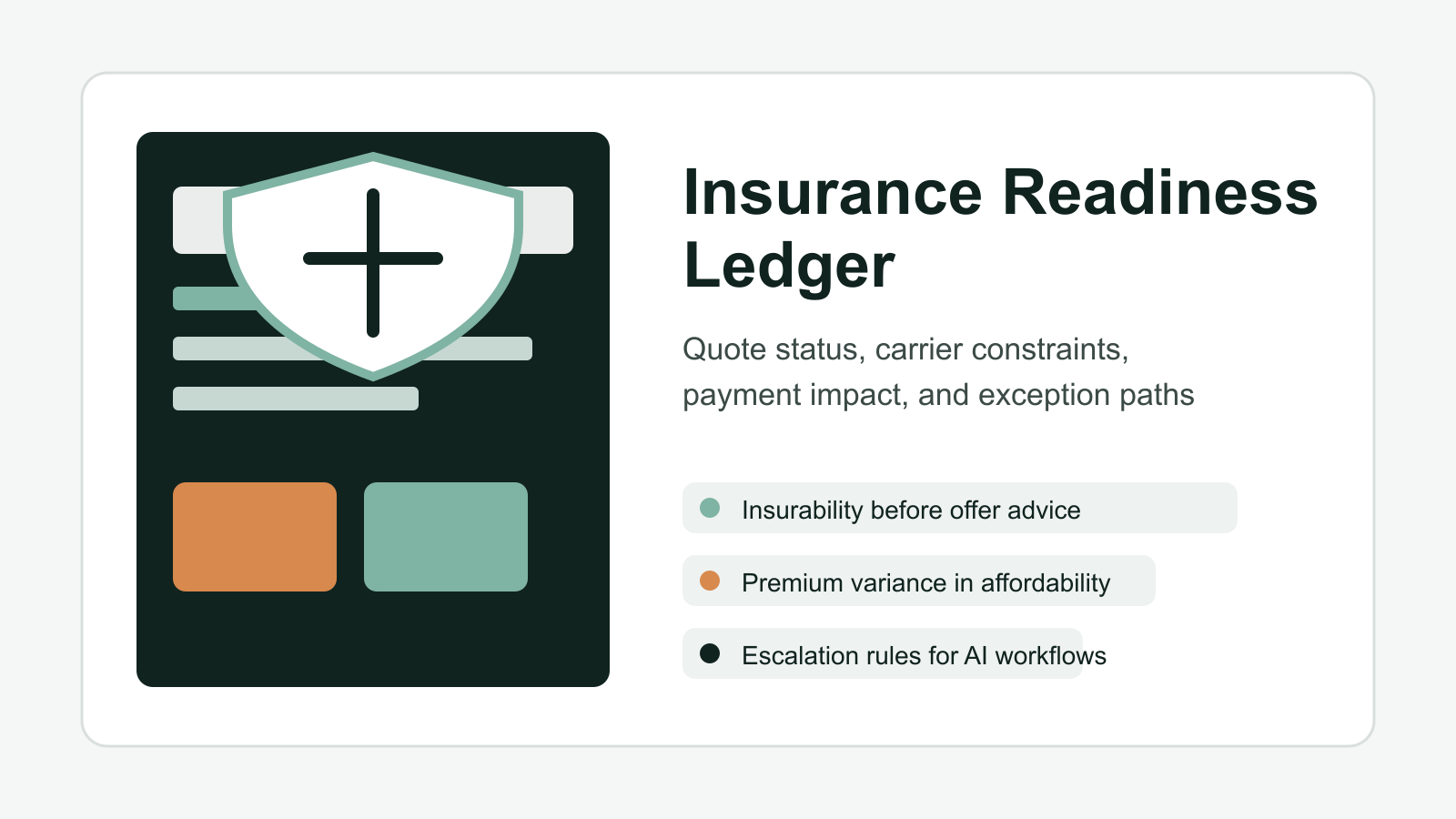

Build an Insurance Readiness Ledger Before AI Advises Offers

Home insurance has moved from closing checklist to deal strategy. A buyer can still like the house, qualify for the loan, and negotiate a fair price, then discover late that the monthly payment no longer works because the insurance quote is higher than the assumptions in the CRM, lender worksheet, or AI-generated offer plan.

That is exactly the kind of operational gap AI will make worse if the brokerage does not structure the data first. An assistant that drafts affordability guidance, offer terms, seller talking points, or post-tour follow-up needs more than price, rate, taxes, and down payment. It needs a live insurance readiness ledger.

Why this belongs in the operating system now

The spring market is showing signs of movement. Redfin reported on April 30, 2026 that U.S. pending sales rose 2.7% year over year during the four weeks ending April 26, while the weekly average mortgage rate fell to 6.23% and the median monthly housing payment moved lower year over year. That creates a tempting message for buyers: affordability is improving, get back in the market.

The problem is that a headline payment is incomplete. NAR's April 15, 2026 insurance-adjusted affordability work shows the standard Housing Affordability Index at 113.7 for March 2026, but the index falls to 109.0 when homeowners insurance is included. That is about a four-point affordability gap from insurance alone compared with the headline view.

The Dallas Fed gives the operational reason this gap is getting harder to ignore. Its April 9, 2026 analysis found that average homeowners insurance premiums for mortgage borrowers rose 62% between 2019 and 2024, with the average mortgaged homeowner spending about $2,300 per year in 2024. The same piece notes that state-level increases were much larger in places like Texas, Florida, Idaho, and Utah.

A separate Dallas Fed analysis from March 24, 2026 connects the insurance line item to credit risk and relocation behavior. It found that national premiums rose about 70% from 2019 to 2025 and that insurance represented 14% of the average monthly payment that includes mortgage principal and interest in 2025, up from 10% in 2013. The authors also found that premium increases can push some borrowers toward credit card reliance, delayed mortgage payments, or relocation.

For a real estate team, this means insurance is no longer a quiet back-office task. It is a buyer qualification variable, a property-selection variable, a seller expectation variable, and an AI safety variable.

What the ledger should capture

The insurance readiness ledger is not a PDF folder. It is a structured record tied to the contact, property, offer, and transaction.

Start with the buyer side. Every active buyer profile should include insurance quote status, quoted annual premium, deductible, carrier, coverage gaps, flood or wind requirements, quote expiration, and whether the quote was used in the lender's latest payment estimate. The important field is not just premium amount. It is confidence level: assumed, quoted, bound, or changed.

Then add property risk context. For each serious property, capture age of roof, major systems age, prior known claims if disclosed, flood-zone review, wildfire or storm exposure flags where relevant, HOA master-policy dependency, and any lender-required coverage notes. Real estate teams do not need to become insurance underwriters, but they do need a clean handoff record before an AI system recommends next steps.

Finally, add workflow status. Who requested the quote? When was it requested? Who received it? Did the buyer understand the payment impact? Did the lender update debt-to-income calculations? Did the agent adjust offer strategy, inspection terms, repair asks, or seller-credit language based on the quote?

Those fields convert insurance from a late surprise into a visible operating signal.

Where AI should use it

Once the ledger exists, AI can help without pretending to be the insurance expert.

In buyer follow-up, AI can summarize the payment impact in plain language and remind the agent which quote is still only an estimate. In offer preparation, AI can flag that the buyer's approval worksheet still uses an assumed premium and should not be treated as final. In seller strategy, AI can identify listings where age, roof condition, or location may create buyer friction and recommend gathering documentation before showings create objections.

The most valuable AI behavior is not automatic advice. It is exception routing.

If the premium is missing, route the file to the buyer agent or lender partner before drafting affordability language. If the premium is materially above the buyer's planning assumption, route the file to a human before suggesting offer terms. If the carrier declines, requires major mitigation, or excludes a coverage category, route the file to a transaction lead before the buyer spends emotional energy on the property.

That is the rule: AI can draft from verified insurance readiness data, but it should escalate when the insurance status is assumed, stale, conflicting, or materially changes affordability.

The CRM implementation

A practical version can be implemented with four linked records.

The contact record stores buyer-level planning assumptions: max comfortable monthly payment, target annual premium range, deductible tolerance, and whether the buyer has preferred insurance contacts. The property record stores risk signals that affect quoting. The offer record stores the quote actually used for the current offer decision. The transaction record stores bound coverage and any post-contract changes.

Do not bury this in notes. Use controlled fields for status and variance. A simple variance field can compare planned premium to quoted premium and categorize the impact: within plan, watch, material change, or deal risk. That one field is enough to power dashboards, task rules, and AI prompts.

The team dashboard should show active buyers with missing quotes, offers using assumed insurance, contracts with unbound coverage, and properties with known insurance friction. This is where the ledger becomes management infrastructure rather than another compliance checklist.

What to tell the team

The message to agents should be direct: do not let AI create payment confidence from incomplete insurance data.

Buyers are hearing that rates have improved and market activity is picking up. That may be true in the aggregate, but the real payment is local, property-specific, and insurance-sensitive. NAR's February 2026 affordability guidance made the same practical point: property taxes, homeowners insurance, utilities, maintenance, and HOA costs belong in the affordability conversation, not after it.

The brokerage that structures this first will give clients better advice and will make its AI systems more useful. The brokerage that ignores it will use AI to polish incomplete assumptions.

The implementation target for this week is small: add insurance readiness fields to the CRM, require quote status before AI-generated offer advice, and build one exception queue for files where premium, coverage, or carrier status changes the buyer's actual payment.

That is enough to turn insurance from a late-stage surprise into an operating signal that agents, lenders, transaction coordinators, and AI can all see.

Written by

Ben Laube

AI Implementation Strategist & Real Estate Tech Expert

Ben Laube helps real estate professionals and businesses harness the power of AI to scale operations, increase productivity, and build intelligent systems. With deep expertise in AI implementation, automation, and real estate technology, Ben delivers practical strategies that drive measurable results.

View full profile