Build an Agentic Payment Approval Ledger Before AI Buys Anything

AI payment infrastructure is moving from demo to operating reality. Visa reported controlled agent-initiated transactions with commerce partners in December 2025 and said it expects AI agents to complete purchases in 2026. In March 2026, Visa also introduced card support for Stripe and Tempo's Machine Payments Protocol, including tokenized card credentials and agent identity verification for programmatic payment workflows. The IMF's April 2026 note on agentic payments frames the same shift more cautiously: payment systems need deterministic authorization, settlement, compliance, and resilience even when the AI system making the request is probabilistic.

That is the practical problem for operators. The risk is not only that an AI agent buys the wrong thing. The risk is that the business cannot prove who authorized the purchase, what limit applied, which system initiated it, what evidence the agent used, and how the transaction should be reversed or disputed. A better model is to build an agentic payment approval ledger before AI receives any card, wallet, billing portal, procurement, or ad-spend authority.

What changed

For the last two years, most business AI work sat upstream of money. A model drafted the email, summarized the lead, compared vendors, wrote the ad, or prepared the invoice. A person still clicked buy, approved spend, or submitted payment. That boundary is weakening.

Stripe and OpenAI's Agentic Commerce Protocol moved checkout into ChatGPT for supported merchants, using a shared payment token so the agentic surface can initiate a payment without exposing raw payment credentials. Google Cloud's Agent Payments Protocol focuses on a traceable chain of intent and payment authorization across agents, merchants, and payment systems. Mastercard's Agent Pay and Visa's agentic commerce work point in the same direction: commerce systems are preparing for non-human actors that can discover, decide, and pay under delegated authority.

The implication for a real estate team, marketing operation, or service business is direct. AI will increasingly sit near ad budgets, vendor renewals, lead-source purchases, listing media orders, software subscriptions, data enrichment credits, transaction services, and client-gift workflows. Those are not abstract payments. They are operational commitments that touch client trust, margin, compliance, and cash flow.

The ledger is the control surface

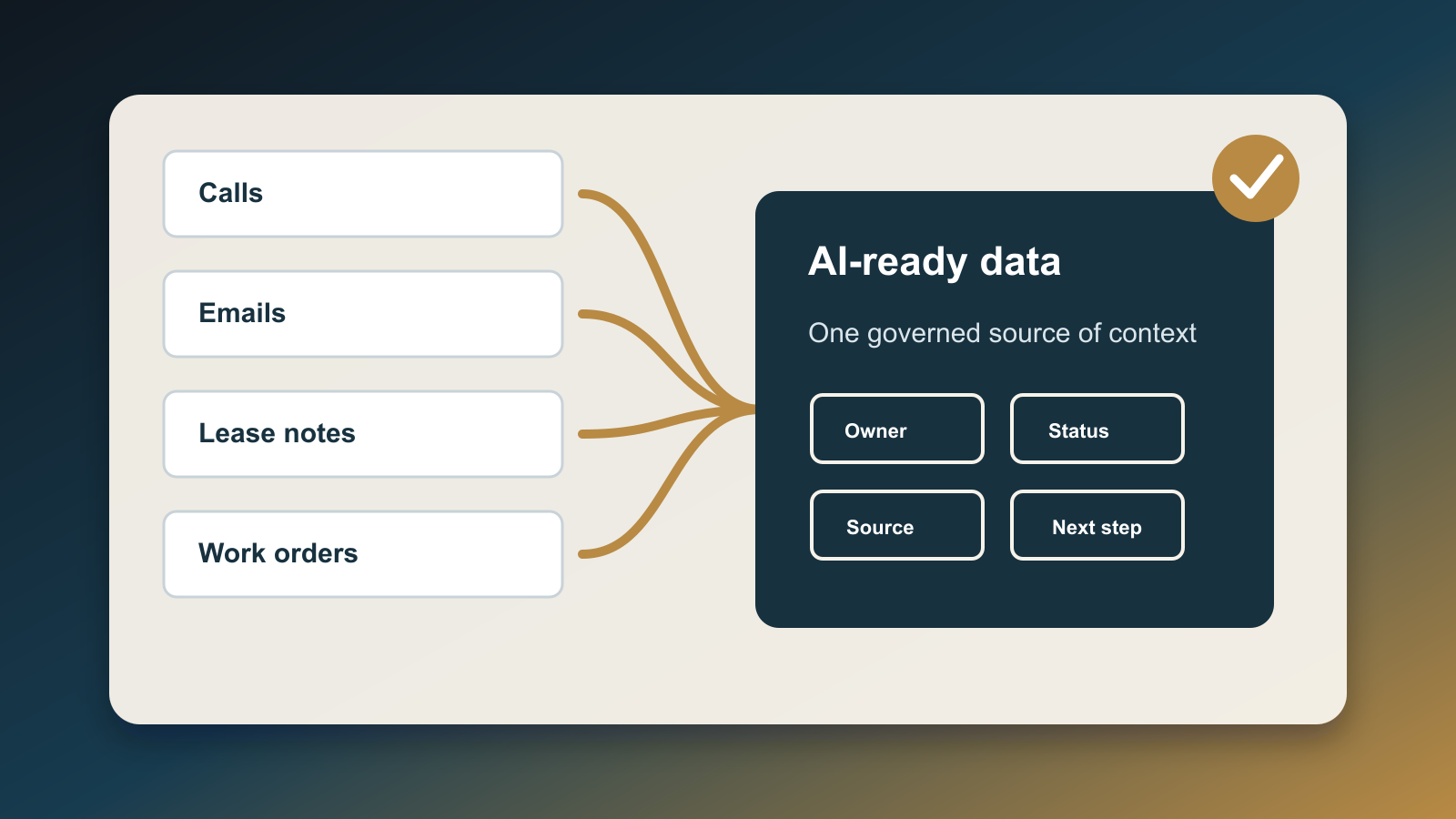

Do not start with the payment rail. Start with the ledger. The ledger is the system of record that says an AI agent may spend only when specific evidence exists.

Each ledger entry should capture seven fields:

- Request: what the agent wants to buy, renew, order, boost, subscribe to, or pay.

- Business reason: the lead, listing, client, campaign, transaction, project, or support case connected to the request.

- Authority: the human owner, approval rule, budget source, and maximum amount.

- Constraints: approved vendors, forbidden categories, geographic or client-specific limits, renewal rules, and expiration date.

- Evidence: quote, invoice, campaign plan, CRM record, source URL, contract, tax document, or internal task that supports the spend.

- Execution record: payment method token, merchant, amount, timestamp, system, agent ID, and confirmation number.

- Exception path: refund owner, dispute owner, pause rule, notification route, and rollback steps.

That sounds heavier than a simple AI workflow. It is intentionally heavier. Any workflow that can spend money needs more friction than a workflow that drafts copy.

Where this matters first

The first use case is ad spend. If an AI marketing system can increase a campaign budget, buy traffic, sponsor a local event, or move money between platforms, the approval ledger should require source quality, audience constraints, fair-housing checks when relevant, channel consent, and a budget cap. The agent can recommend a spend change, but it should not execute without a matching ledger entry.

The second use case is software and data credits. AI agents will consume APIs, enrich CRM records, buy compute, and renew SaaS tools. Visa's Machine Payments Protocol update is a reminder that agent payments are not limited to consumer checkout. Command-line and machine-to-machine commerce are part of the same trend. For a business, that means the approval ledger needs spend ceilings by workflow, not just by company card.

The third use case is vendor coordination. A transaction coordinator might ask AI to order photography, schedule cleaning, request signage, pay a contractor deposit, or buy a closing gift. Some of those are harmless. Some are contractual, client-sensitive, or reimbursement-sensitive. The ledger should know the difference.

The fourth use case is invoice triage. AI can read an invoice, match it to a job, and recommend payment. It should also detect missing purchase orders, changed bank details, new vendors, duplicate invoice numbers, and amounts outside normal range. Those exceptions should route to a person before money moves.

How to implement it without overbuilding

A small team does not need a new finance platform to begin. Add a table or board with status values: requested, approved, executed, exception, reversed, and closed. Connect each row to the CRM record, campaign, client file, or project that created the need. Require a human owner and a budget limit before any agent can act.

Then separate recommendation from execution. The AI can research options, fill the request fields, attach evidence, and prepare the payment instruction. Another rule decides whether the agent can execute automatically, whether it needs one-click approval, or whether it must stop for manual review.

Use narrow tokens instead of broad credentials wherever the payment provider supports them. The important principle is scope. A token that can pay one approved merchant up to one approved amount is safer than a card saved inside a browser profile. When scope is not available, reduce agent authority. Let it prepare the work, not perform the purchase.

Finally, audit the ledger weekly. Look for requests without evidence, repeated exceptions, auto-approved spend that never produced a business outcome, and workflows where the agent keeps asking for broader authority. Those findings are not paperwork. They are the roadmap for safer automation.

The operating rule

Agentic commerce will make buying feel like another software action. That is useful, but it changes the control problem. A business should not ask, "Can the AI pay?" first. The better question is, "What must be true before the AI is allowed to spend?"

If the answer lives only in a prompt, it is not a control. Put it in a ledger. Tie every purchase to intent, authority, evidence, execution, and exception handling. Then AI can help with payments without turning every workflow into an untraceable expense account.

Sources

- Visa, "Visa and Partners Complete Secure AI Transactions, Setting the Stage for Mainstream Adoption in 2026," December 18, 2025: https://usa.visa.com/about-visa/newsroom/press-releases.releaseId.21961.html

- Visa, "Visa introduces card specification and SDK for Machine Payments Protocol," March 18, 2026: https://corporate.visa.com/en/sites/visa-perspectives/innovation/visa-card-specification-sdk-for-machine-payments-protocol.html

- International Monetary Fund, "How Agentic AI Will Reshape Payments," April 24, 2026: https://www.imf.org/en/publications/imf-notes/issues/2026/04/22/how-agentic-ai-will-reshape-payments-575560

- Google Cloud, "Announcing Agent Payments Protocol (AP2)," September 16, 2025: https://cloud.google.com/blog/products/ai-machine-learning/announcing-agents-to-payments-ap2-protocol

- Stripe, "Stripe powers Instant Checkout in ChatGPT and releases Agentic Commerce Protocol codeveloped with OpenAI," September 29, 2025: https://stripe.com/newsroom/news/stripe-openai-instant-checkout

- Mastercard press release index, "Mastercard unveils Agent Pay," April 29, 2025: https://www.mastercard.com/us/en/news-and-trends/press.html

Written by

Ben Laube

AI Implementation Strategist & Real Estate Tech Expert

Ben Laube helps real estate professionals and businesses harness the power of AI to scale operations, increase productivity, and build intelligent systems. With deep expertise in AI implementation, automation, and real estate technology, Ben delivers practical strategies that drive measurable results.

View full profile