Build a Special-Assessment Tracker Before AI Advises Condo Buyers

Special assessments are one of the easiest places for AI to sound useful while creating real transaction risk. A buyer asks whether a condo is still affordable. A seller asks whether the pending roof project needs to be mentioned. An agent asks the CRM to draft a quick answer from the resale package. The model sees board minutes, dues, a reserve number, and a few notes, then turns that into confident language before the team has separated verified facts from lender, legal, and disclosure questions.

That is the wrong operating order. Real estate teams should build a special-assessment tracker before they let AI advise condo buyers, answer HOA questions, or summarize seller risk.

The current lending and buyer-education sources make the reason clear. Fannie Mae's project-eligibility guidance treats current and planned special assessments as review items, especially when they relate to critical repairs. Its appraisal guidance for special assessment or community facilities districts also expects lenders and appraisers to consider how assessments can affect property value and marketability. The Foundation for Community Association Research explains the plain-language distinction: regular assessments fund normal operations and reserves, while special assessments are one-time charges when reserves or insurance are not enough for a project or unexpected expense.

That combination is exactly where automation needs a structured gate. AI should not be the first system to decide whether an assessment is routine, critical, paid, planned, collectible, lender-sensitive, disclosure-sensitive, or outside the team's lane.

The Tracker Is an Evidence Gate

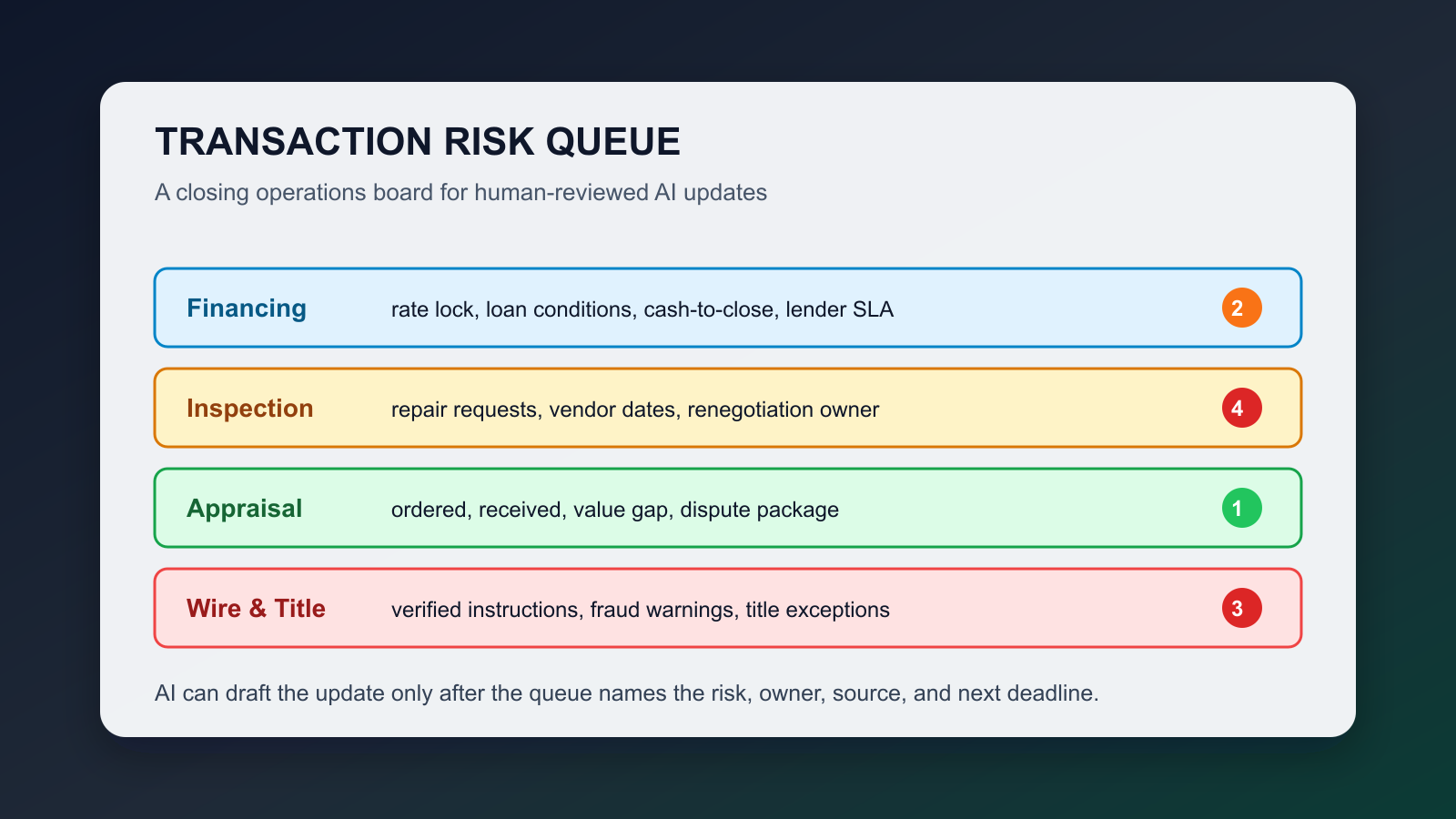

A useful tracker is not another note field called HOA issue. It is a small operating table that forces the team to record the facts a human reviewer would need before client-facing language goes out.

Start with the assessment identity: project name, unit address, association or district name, property manager contact, board contact, and source document. Then capture the decision status: rumored, board-discussed, board-approved, owner-approved if required, collection initiated, partially collected, paid in full, cancelled, or superseded. That status matters because a loose note that says possible assessment should not produce the same AI answer as an approved special assessment with a payment schedule.

The second layer is money. Track the original amount, per-unit allocation, remaining amount, payment frequency, first due date, expected payoff date, whether the subject unit has paid anything, and whether the assessment has more than a short remaining term. Do not force AI to infer affordability impact from a PDF paragraph. Give it a clean number, a source, and a timestamp.

The third layer is purpose. Use controlled categories: routine reserve catch-up, capital improvement, critical repair, insurance shortfall, code or inspection issue, litigation settlement, utility district or infrastructure assessment, operating deficit, or unknown. The purpose is the routing key. A pool resurfacing project, a fire-safety repair, and a municipal utility district assessment may all use similar words but require different reviewers.

The fourth layer is source quality. The tracker should point to board minutes, resale certificate, budget, reserve study, engineer report, structural or mechanical inspection report, association statement, tax bill, lender questionnaire, seller disclosure, or attorney note. Fannie Mae's ineligible-project guidance lists documents lenders may need to review, including HOA board minutes, engineer reports, reserve studies, necessary repair lists, and special-assessment lists. The AI workflow should know which of those documents are present and which are missing before it answers.

Where AI Is Allowed to Help

Once the tracker exists, AI becomes useful in narrower and safer ways.

It can summarize a verified assessment record in plain language for the agent. It can create a checklist of missing documents. It can draft a buyer question list for the lender, the association, or the attorney. It can compare the resale package against the tracker and flag mismatches: payment schedule missing, board approval date absent, purpose unknown, reserve study older than the file expects, or status not updated after new minutes arrived.

It should not decide whether the assessment is legally disclosable, whether a buyer should proceed, whether the project is warrantable, whether the seller must pay at closing, or whether a lender will approve the project. Those are routing outcomes, not model outputs.

A practical permission model is simple:

- Answer: AI may summarize verified facts already approved for client communication.

- Hold: AI may draft internal notes, but client-facing language waits for a human owner.

- Escalate: AI must route to lender, broker, attorney, association manager, appraiser, or another qualified reviewer.

- Block: AI must not generate advice because the assessment purpose, amount, source, or status is unknown.

This is consistent with broader AI risk practice. NIST's AI Risk Management Framework is built around mapping, measuring, managing, and governing risk. In a brokerage workflow, that does not require a big compliance program. It means the system must know what fact it is using, what decision it is supporting, what harm could happen if the fact is wrong, and who has authority to approve the answer.

The Minimum Fields

A special-assessment tracker should be boring enough that agents actually maintain it.

Use these fields:

- Property and association: address, project name, association or district, manager contact.

- Assessment status: rumored, discussed, approved, collecting, paid, cancelled, unknown.

- Approval evidence: board date, owner vote date if applicable, document link, source owner.

- Financial terms: original total, per-unit share, remaining amount, due dates, payment schedule, payoff target.

- Purpose: routine, capital, critical repair, insurance, litigation, utility district, operating shortfall, unknown.

- Physical-condition connection: engineer report, inspection report, reserve study, code notice, repair list.

- Transaction impact: buyer affordability, seller net, lender review, appraisal value or marketability, closing allocation, disclosure review.

- AI permission: answer, hold, escalate, block.

- Reviewer and timestamp: accountable human, last reviewed date, next review trigger.

The field that changes behavior is AI permission. Without it, the model will treat every row as usable context. With it, the CRM can filter what the model sees, show safer snippets, and stop the draft when a missing field matters.

How to Use It in a Transaction

For a buyer, the tracker should produce a concise internal brief before any client answer: what is known, what is unknown, what documents support the record, and who needs to review it. If the assessment is approved but collection has not started, the answer should say the team has an approved assessment record and is routing payment and financing questions to the right reviewer. It should not imply the buyer's lender will ignore it.

For a seller, the tracker should connect the assessment to listing prep, seller net, and disclosure review. The AI can prepare a document checklist and a plain-language draft for the agent, but the broker or attorney path should control final guidance where state law, contract terms, or association documents drive the answer.

For an operations leader, the tracker becomes a management report. Which listings have unknown assessment status? Which buyer files are waiting on resale packages? Which projects mention critical repairs? Which assessments have no source document? Which AI drafts were blocked because the field owner had not reviewed the record?

That is the real benefit. The team stops treating special assessments as inbox surprises and starts treating them as governed transaction facts.

The Implementation

Put the tracker in the CRM or transaction workspace, not in a separate spreadsheet that automation cannot read. Attach every source document to the record. Require a status, purpose, amount, source, reviewer, and AI permission before the record becomes eligible for AI summaries. Add a stale-date rule so board minutes, budgets, payment status, and resale-package facts do not live forever.

Then wire the AI prompt to the tracker instead of to the whole document folder. The prompt should say: summarize only fields marked answer; list missing fields for anything marked hold; route anything marked escalate; refuse to advise when status or source is unknown.

Real estate teams are adopting AI because it saves time, and NAR's 2025 Technology Survey shows AI-generated content is already part of many agents' toolkits. But condo assessments are not just content. They touch affordability, project health, marketability, lender review, seller communication, and buyer confidence.

The practical rule is simple: if the answer could change a buyer's cost, a seller's net, or a lender's view of the project, AI needs a verified assessment tracker first.

Written by

Ben Laube

AI Implementation Strategist & Real Estate Tech Expert

Ben Laube helps real estate professionals and businesses harness the power of AI to scale operations, increase productivity, and build intelligent systems. With deep expertise in AI implementation, automation, and real estate technology, Ben delivers practical strategies that drive measurable results.

View full profile