Build a Transaction Risk Queue Before AI Updates Closings

AI can draft closing updates quickly. That is useful, but it is also dangerous when the underlying transaction record is scattered across texts, lender portals, inspection notes, title emails, calendar holds, and agent memory. A clean update is not the same as a safe update. In a real estate transaction, the client needs to know what changed, who owns the next step, what deadline matters, and whether the deal is actually at risk.

The practical move is to build a transaction risk queue before letting AI write closing updates. The queue is a shared operating board that turns every open risk into a structured record: issue type, source, severity, owner, deadline, client impact, next action, and approved message. AI can summarize that board. It should not be guessing from raw inbox fragments.

Closings still have real friction

The current market gives teams a good reason to tighten closing operations. NAR's latest Realtors Confidence Index reports that contracts typically closed in 30 days, but 5% of contracts were terminated in the prior three months, 13% had delayed settlements, and 7% were delayed because of appraisal issues. NAR also reported that fewer buyers waived inspection and appraisal contingencies than in the prior month, which means more transactions still contain explicit due diligence checkpoints.

That does not mean every deal is fragile. It means the fragile ones need visibility before the next client update goes out. A buyer who receives a confident AI-written progress note while the appraisal is late, the title exception is unresolved, or the insurance quote is about to change will remember the false confidence more than the wording quality.

Market conditions add another layer. NAR's April 13, 2026 existing-home sales release showed March sales down 3.6% from February, inventory up to 4.1 months of supply, and the median price still rising year over year. The same release said rising mortgage rates led NAR to trim its 2026 sales forecast. Meanwhile, MBA's April 29, 2026 weekly survey reported a 1.6% weekly drop in mortgage applications, even as the purchase index rose from the prior week and stood above the year-earlier level on an unadjusted basis. That mix is exactly why closing communication needs operational context: demand is not dead, but financing and timing remain variable.

The risk is not only delay

Most teams think of closing risk as a calendar problem. The better frame is operating risk. Financing risk, appraisal risk, inspection risk, insurance risk, title risk, wire fraud risk, occupancy risk, document risk, and communication risk all behave differently. They have different owners and different approved language.

Wire and title issues deserve special treatment. The FBI's 2025 Internet Crime Report, released in April 2026, said cyber-enabled crimes produced nearly $21 billion in losses reported to IC3, and the FBI highlighted compromised corporate email and AI-enabled deception among the tactics. ALTA's 2025 cybercrime study reported that more than 40% of title companies received at least one monthly attempt to change wiring or payoff instructions in 2023, and it emphasized consumer education, staff training, and wire/payee verification as risk controls.

That belongs in the same operating system as inspection and appraisal. If an AI assistant is allowed to send closing updates, it must know which wire instructions have been verified, which communication channel is approved, and which phrases are forbidden. It should never improvise around funds, title, payoff, or wiring language.

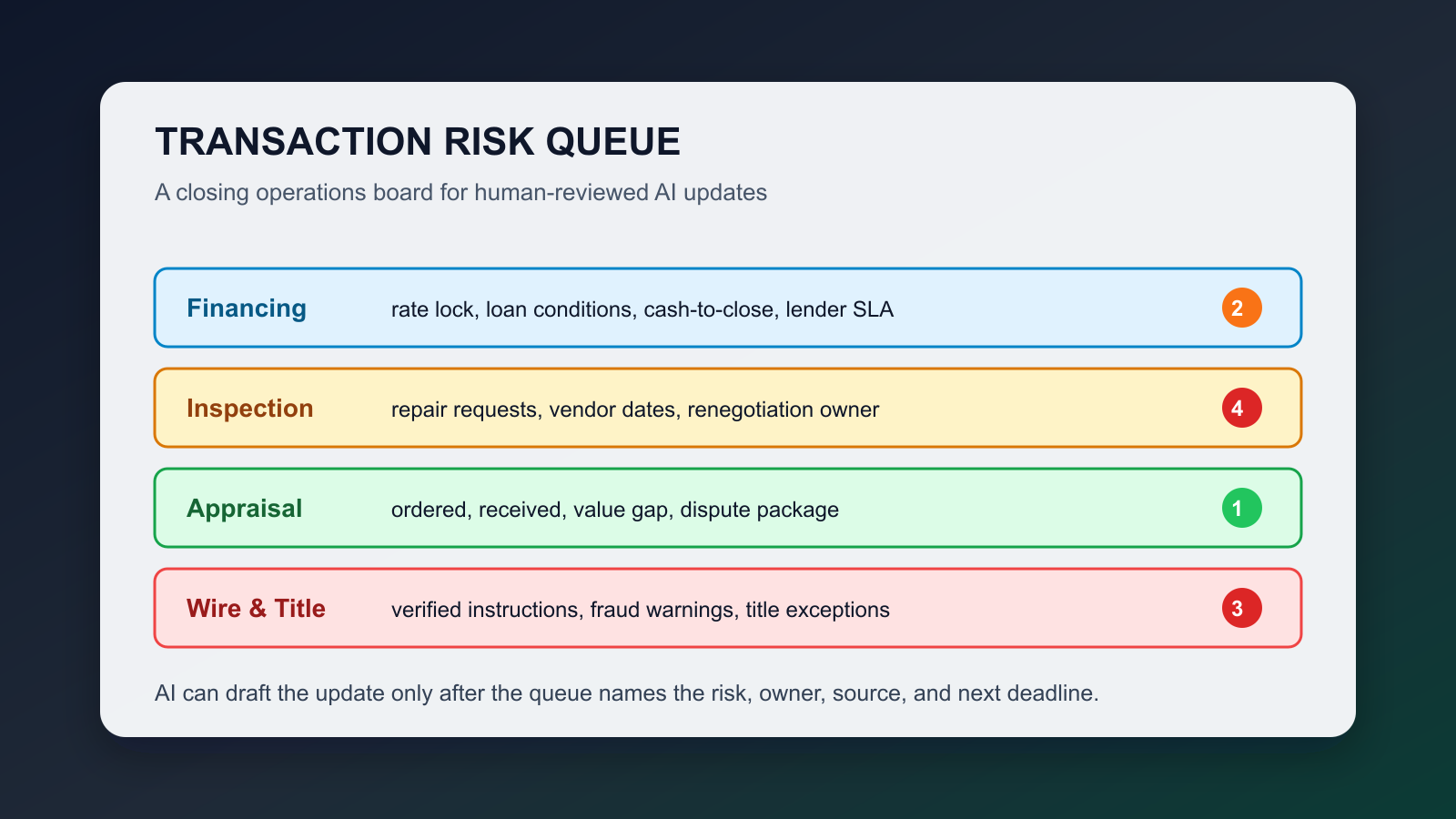

What belongs in the queue

Start with a simple transaction risk table. Each row should include transaction ID, property, client side, milestone, risk category, status, severity, source, owner, due date, last verified timestamp, client-facing summary, internal notes, escalation flag, and approved next message.

Use five severity levels. Green means the milestone is complete or on track. Watch means a dependency exists but the owner has a date. Blocked means the next milestone cannot move until someone acts. Client decision means the buyer or seller must choose. Escalate means legal, broker, lender, title, wire, fair housing, safety, or material contract risk is present.

Then define the source rules. A financing risk should point to a lender update or documented condition list, not hearsay. An appraisal risk should point to ordered, scheduled, received, value gap, reconsideration, or cleared. An inspection risk should point to report received, repair request drafted, negotiation open, vendor quote needed, or resolved. A title risk should point to title commitment status, exceptions, payoff, lien release, HOA, probate, entity authorization, or closing protection issue. A wire risk should point only to verified instructions and approved fraud-warning language.

The queue should also separate internal truth from client language. Internal notes can say the seller is frustrated, the lender missed a deadline, or the repair estimate is unclear. Client language should say what is verified, what happens next, and when the next update will come. AI is valuable here because it can turn structured facts into clear messages. It is risky when it compresses uncertainty into confidence.

Give AI a narrow job

The AI prompt should receive the queue record, not the whole messy transaction history. It should be told the client side, risk level, approved facts, prohibited claims, next deadline, and desired tone. The output should be a draft update plus a confidence note that says what evidence it used.

For green and watch items, AI can usually draft the first version. For blocked, client decision, or escalate items, AI can summarize the facts and propose questions, but a human should approve the message before it leaves the team. For wire, title, legal, lending, contract, inspection defect, insurance, or safety language, require human approval every time.

A useful rule is simple: AI may explain the status, but it may not create the status. If the queue does not show that a condition is cleared, AI cannot say it is cleared. If the queue does not show verified wire instructions, AI cannot reference instructions. If the queue does not show a confirmed date, AI cannot promise one.

The minimum weekly operating rhythm

Run a transaction risk review every morning during active closings. It does not need to be a long meeting. Review only four buckets: new risks, overdue risks, client-decision risks, and escalations. Every row must leave the review with an owner, next action, deadline, and message status.

After that review, AI can help draft the day's client updates. The human operator should scan for three things: unsupported certainty, missing deadline, and wrong owner. If those are clean, the message can go out. If not, the record gets fixed before the message gets polished.

At the end of each closing, tag the resolved risks. Which ones were predictable? Which ones were avoidable? Which vendor, lender, source, property type, or price band created recurring delays? That history becomes the training data for better checklists, better partner scorecards, and better future AI triage.

Bottom line

A closing update is only as good as the transaction system behind it. AI can make the message faster, clearer, and more consistent, but it cannot replace the operating discipline that says what is true, what is uncertain, who owns the next step, and what should be escalated.

Build the transaction risk queue first. Then let AI draft inside it. The result is not just better communication. It is fewer surprise escalations, cleaner handoffs, and a closing process where clients hear confidence only when the team has earned it.

Sources

- National Association of REALTORS, Realtors Confidence Index Report, accessed May 2, 2026: https://www.nar.realtor/research-and-statistics/research-reports/realtors-confidence-index

- National Association of REALTORS, Existing-Home Sales Report Shows 3.6% Decrease in March, April 13, 2026: https://www.nar.realtor/newsroom/nar-existing-home-sales-report-shows-3-6-decrease-in-march

- Mortgage Bankers Association, Mortgage Applications Decrease in Latest MBA Weekly Survey, April 29, 2026: https://www.mba.org/news-and-research/newsroom/news/2026/04/29/mortgage-applications-decrease-in-latest-mba-weekly-survey

- Federal Bureau of Investigation, Cryptocurrency and AI Scams Bilk Americans of Billions, April 6, 2026: https://www.fbi.gov/news/press-releases/cryptocurrency-and-ai-scams-bilk-americans-of-billions

- American Land Title Association, Title Companies Help Mitigate Risk of Wire Fraud, ALTA Cybercrime Study Shows, February 27, 2025: https://www.alta.org/news-and-publications/news/20250227-Title-Companies-Help-Mitigate-Risk-of-Wire-Fraud-ALTA-Cybercrime-Study-Shows

Written by

Ben Laube

AI Implementation Strategist & Real Estate Tech Expert

Ben Laube helps real estate professionals and businesses harness the power of AI to scale operations, increase productivity, and build intelligent systems. With deep expertise in AI implementation, automation, and real estate technology, Ben delivers practical strategies that drive measurable results.

View full profile