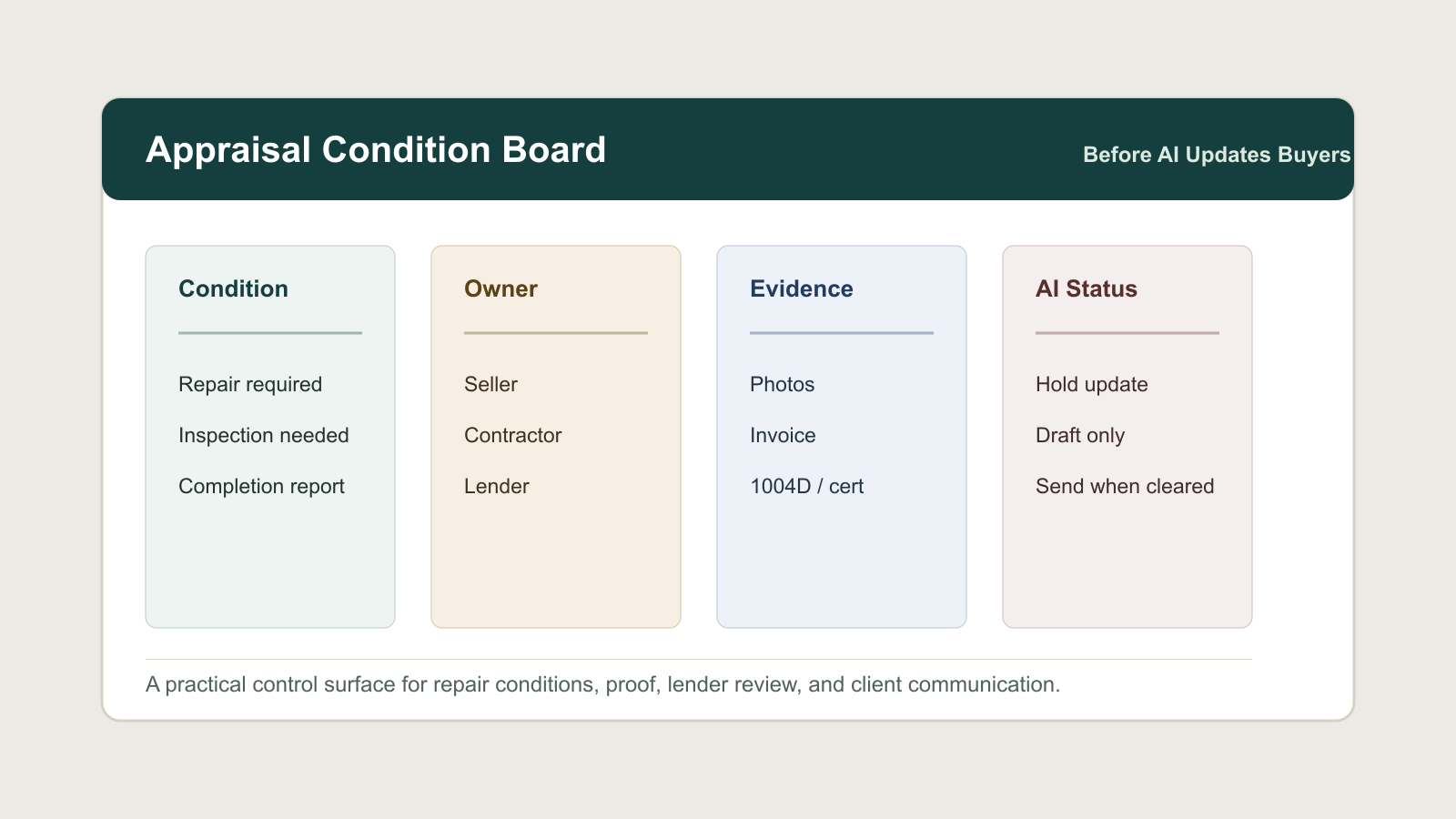

Build an Appraisal Condition Board Before AI Updates Buyers

AI is useful when buyers want a plain-language update after the appraisal comes back. It can summarize a lender note, draft a text message, or turn a repair condition into a closing checklist. The risk is that the model may sound confident before the condition is actually cleared.

That is the wrong failure mode. An appraisal condition is not a normal task reminder. It can touch the lender, appraiser, seller, buyer, contractor, listing agent, buyer agent, and closing timeline. If the team lets AI summarize from a messy email thread, it can blur the difference between "repair requested," "repair completed," "evidence uploaded," and "lender accepted."

A small appraisal condition board fixes that. It gives the team one controlled place to track the condition, the owner, the proof, the required review, and the communication status before any AI assistant updates the buyer.

Why this deserves its own workflow

Fannie Mae's property-condition guidance makes the operational issue clear: appraisers must identify needed repairs and physical deficiencies that affect safety, soundness, or structural integrity, and some reports are completed subject to repairs, alterations, or a satisfactory inspection by a qualified professional. Fannie Mae's completion guidance also points to evidence of completion and completion reports, including Form 1004D, when appraisal requirements or conditions have been met.

FHA and VA files can add their own vocabulary. HUD's Single Family Housing Policy Handbook 4000.1 is the consolidated FHA policy source, and the VA Lender's Handbook includes minimum property requirement chapters and appraisal handling. A brokerage team does not need to turn every coordinator into an underwriter. It does need a clean evidence trail so nobody mistakes a contractor photo for lender clearance.

That matters more as agents adopt AI. NAR's 2025 technology survey reported broad use of digital tools and meaningful AI adoption among REALTORS. NIST's AI Risk Management Framework pushes teams toward trustworthy, accountable, and reliable AI use. In a transaction workflow, that means AI should not be the system of record for appraisal conditions. It should read from one.

The board structure

Keep the board boring. The goal is not another CRM shrine. The goal is a short set of fields that prevent premature communication.

Use these columns:

- Property and transaction ID

- Loan type or appraisal context, when known

- Condition source: appraisal report, lender note, underwriter request, appraiser comment, or buyer-side observation

- Exact condition text copied from the source document

- Required next action

- Owner: seller, buyer, listing agent, buyer agent, contractor, lender, appraiser, or escrow/title

- Due date and closing impact

- Evidence required

- Evidence received

- Review required: appraiser, lender, qualified professional, internal broker review, or none

- Clearance status

- AI communication status

The most important field is clearance status. Use a controlled list, not free text:

- New condition

- Assigned

- Evidence pending

- Evidence uploaded

- Review requested

- Cleared by lender or appraiser

- Blocked

- Not cleared, do not update buyer as resolved

That last status is useful because it forces the assistant and the human team to say the quiet part out loud. A repair may look done. It may still not be cleared.

What AI can and cannot do

AI can help translate the board into client-ready language. It can prepare a short update such as: "The repair evidence has been uploaded and the lender review is pending." It can also generate internal reminders, summarize the open blockers, and flag stale conditions.

It should not decide whether the property satisfies loan requirements. It should not infer that a condition is cleared because someone attached photos. It should not send the buyer a closing-confidence message until the board says the required review is complete.

A simple rule works: if clearance status is anything other than "Cleared by lender or appraiser," AI may draft but not send resolved language.

The evidence packet

The board should link to a packet, not scatter proof across inboxes. For each condition, collect:

- The source excerpt from the appraisal or lender request

- Contractor estimate or invoice, if relevant

- Before and after photos, if relevant

- Permit, specialist report, pest letter, roof note, foundation note, or other professional documentation, if relevant

- Completion report or lender/appraiser acceptance, when required

- Date the proof was sent

- Date the proof was accepted

Do not let the AI assistant summarize attachments it cannot actually access. If a document is missing, the update should say it is missing. If a document is present but not reviewed, the update should say it is awaiting review.

Implementation in a week

Start with a spreadsheet, Airtable base, CRM custom object, or transaction-management checklist. The tool matters less than the status discipline.

Day one: define the statuses and owners. Day two: add the required fields and create a condition intake form. Day three: connect document links. Day four: write three AI prompts that read only from the board: buyer update, internal blocker summary, and closing-risk note. Day five: test the prompts against two old transactions where conditions were messy.

The test is simple. Can the assistant distinguish these four states?

- The repair was requested.

- The repair was completed.

- Evidence was submitted.

- The condition was cleared.

If the answer is no, the workflow is not ready for client-facing automation.

A practical prompt guardrail

Use a prompt rule like this:

"You are drafting a transaction update from the appraisal condition board. Do not say a condition is complete, resolved, approved, or cleared unless clearance_status equals 'Cleared by lender or appraiser.' If evidence is uploaded but review is pending, say review is pending. If required evidence is missing, list the missing evidence. Do not provide lending, appraisal, repair, legal, or tax advice."

Then add a human review gate for any buyer-facing message where closing impact is marked high, where the loan type has special property requirements, or where the evidence packet includes specialist reports.

The business payoff

This is not just compliance hygiene. It reduces duplicate calls, anxious buyer updates, lender back-and-forth, and last-minute blame. It also makes the team faster because every person can see the same operational truth.

When the board is clean, AI becomes useful in the right way. It can compress the status, draft the update, and remind the owner. The team still controls the facts, the clearance threshold, and the client promise.

That is the pattern worth repeating across real estate operations: before AI communicates a sensitive transaction status, build the evidence board that tells it what is actually true.

Sources

- Fannie Mae Selling Guide: Property Condition and Quality of Construction

- Fannie Mae Selling Guide: Requirements for Verifying Completion and Postponed Improvements

- HUD: FHA Single Family Housing Policy Handbook 4000.1

- VA Lender's Handbook, VA Pamphlet 26-7

- NAR: REALTORS Embrace AI, Digital Tools to Enhance Client Service

- NIST AI Risk Management Framework

Written by

Ben Laube

AI Implementation Strategist & Real Estate Tech Expert

Ben Laube helps real estate professionals and businesses harness the power of AI to scale operations, increase productivity, and build intelligent systems. With deep expertise in AI implementation, automation, and real estate technology, Ben delivers practical strategies that drive measurable results.

View full profile