Build an Earnest Money Risk Ledger Before AI Explains Deposits

AI can make deposit questions sound simple. That is exactly why real estate teams need an earnest money risk ledger before an assistant explains what a buyer has paid, what happens if a deal stalls, or whether a deposit is likely to be returned.

Earnest money sits in a risky middle ground. It is operational enough that clients ask about it constantly, financial enough that lenders may need documentation, and contract-specific enough that a confident generic answer can create real harm. A model can summarize a transaction note, but it should not decide whether a missed deadline, failed contingency, changed instruction, or canceled contract changes the client’s rights.

A better pattern is to make the ledger the source of truth and let AI draft only from approved fields. The ledger does not replace the contract, broker, escrow holder, lender, or attorney. It gives the team a clean operating surface so deposit communication is fast without becoming casual.

Why This Needs a Ledger

The National Association of REALTORS consumer guide explains escrow and earnest money as part of the period between signing and closing, with funds commonly held by a third party until contract terms are met or a dispute is resolved. That single point matters operationally: the deposit is not just a line in a CRM note. It has a holder, a receipt, contract terms, and a status that can change when contingencies are satisfied, waived, disputed, or missed.

Fannie Mae’s selling guide also treats earnest money as a documented funds item. When the deposit is used toward the borrower’s required contribution, the lender may need verification of the source of funds and evidence that the money changed hands. That turns the team’s deposit tracking into more than client service. It affects loan packaging, document requests, and closing readiness.

CFPB closing guidance reinforces the same discipline from the consumer side: buyers should review closing documents in advance and understand the documents and payment obligations before closing. The FTC’s wire-transfer guidance adds the practical fraud risk: once money is wired to the wrong place, recovery can be difficult or impossible. Those facts make AI-generated deposit explanations useful only when the underlying evidence is current, scoped, and reviewed.

Meanwhile, AI is already part of real estate operations. NAR’s 2025 technology survey found broad use of digital tools and meaningful adoption of AI-generated content among agents. NIST’s AI Risk Management Framework pushes organizations to manage AI risk across design, use, measurement, and oversight. For a brokerage or team, the translation is straightforward: do not let the model improvise on financial, contractual, or fraud-sensitive deposit issues.

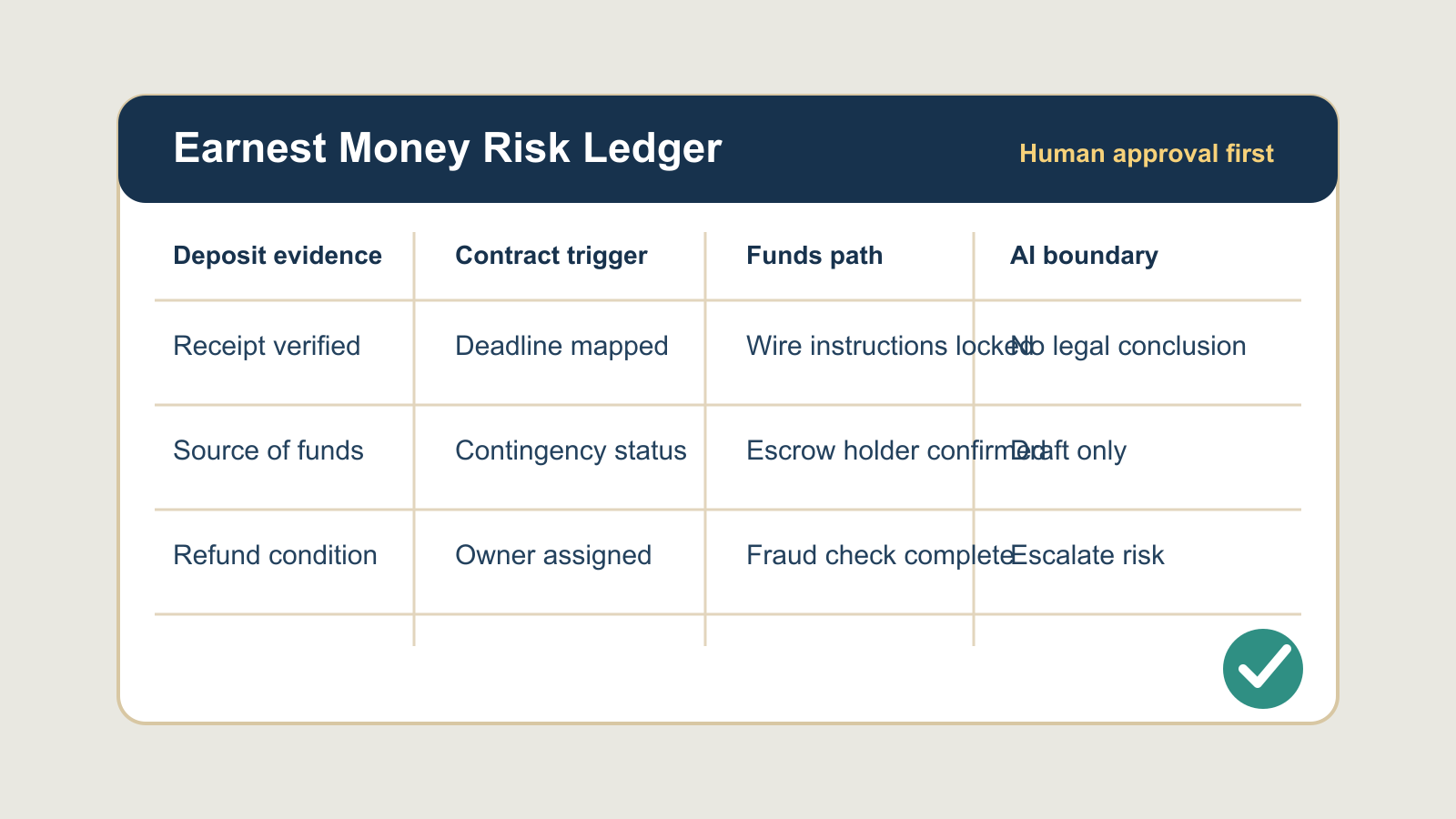

What the Ledger Should Track

Start with the deposit itself. Record the agreed amount, due date, method, payer, escrow holder, receipt status, and the document that proves it. The evidence should be specific: receipt, canceled check, bank confirmation, escrow email, settlement platform confirmation, or lender-accepted documentation. A note that says “EMD sent” is not enough for automation.

Then map the contract context. The ledger should show which agreement controls the deposit, which contingencies may affect it, which deadlines matter, and who owns interpretation. This does not mean the AI system interprets the contract. It means the model can see whether the deposit question is routine, unresolved, or escalated.

Add a funds-path section. This is where the team records whether payment instructions came from the verified escrow or settlement contact, whether the buyer independently confirmed instructions, and whether any last-minute change has been approved by a human. This section should be locked down. AI can remind a client to verify instructions through the approved channel, but it should not generate new wire instructions, forward account details, or paraphrase a payment route from an email thread.

Finally, add an answer boundary. Every deposit row should have one of four statuses: explainable, draft-only, needs broker review, or needs legal/escrow/lender review. This field is the difference between helpful automation and a risky hallucination. If the ledger says “needs review,” the assistant stops at intake and routing.

Where AI Can Help Safely

AI is useful for first-pass organization. It can extract the deposit amount from a signed agreement, compare the due date with a transaction calendar, flag missing receipt evidence, summarize the current status for an internal dashboard, and draft a plain-language message that asks for a missing document.

It can also help prevent communication drift. If the buyer asks, “Do I lose my deposit if we cancel?” the model should not answer from memory or local custom. It should read the ledger and produce a bounded response: the question depends on the signed contract, current contingency status, and any escrow or legal guidance; the team is reviewing the file; no conclusion should be treated as final until the responsible human confirms it.

That may sound slower than a direct answer. In practice, it is faster because the assistant can gather the right facts immediately instead of generating confident language that a broker has to unwind later.

The Operating Workflow

Use a five-step workflow.

First, create the deposit row as soon as the offer is accepted. Do not wait for a client question. The row should be tied to the transaction ID, buyer, property, escrow holder, responsible agent, and contract version.

Second, verify the receipt. The team should not mark the deposit as complete until the evidence is attached or linked. If the receipt is missing, AI may draft a reminder, but the reminder should name only the approved recipient and avoid payment instructions unless those instructions come from a controlled template reviewed by the team.

Third, reconcile the ledger with financing. If the lender needs source-of-funds documentation, the row should show that status separately from the escrow receipt. A buyer can have delivered the deposit and still need lender documentation. AI should not collapse those into one “done” state.

Fourth, review risk before client-facing explanations. Questions about refunds, forfeiture, extensions, missed deadlines, cancellations, or disputed funds should automatically route to the broker, attorney, escrow holder, or lender depending on the issue. The AI draft can organize facts, but it should not decide rights.

Fifth, close the loop after settlement or cancellation. Mark whether the deposit was credited, returned, disputed, or otherwise resolved, and retain the final evidence. This makes future client service cleaner and reduces the temptation to infer from old notes.

A Practical Data Model

A lightweight ledger can live in the CRM or transaction management system. The minimum fields are:

- Transaction ID

- Buyer and property

- Deposit amount and due date

- Escrow holder and verified contact method

- Payment method category, without exposed account details

- Receipt evidence link

- Lender documentation status

- Contract contingency flags

- Human owner

- AI answer boundary

- Last reviewed timestamp

- Resolution status

The key is not the tool. The key is field discipline. AI systems fail in operational settings when the business asks them to turn messy notes into confident action. They perform better when the business gives them structured states, evidence links, and clear escalation rules.

What Not To Automate

Do not automate legal conclusions about who gets the deposit. Do not let an assistant rewrite wire instructions from an email. Do not let it tell a buyer that funds are safe simply because a message appears to come from a familiar party. Do not let it mark a deposit complete without receipt evidence. Do not let it reuse a past transaction’s contingency logic.

The safest AI pattern is conservative: collect facts, compare required fields, draft non-final language, and escalate ambiguity. That still saves time. It just saves time in the part of the work where automation belongs.

The Implementation Test

Before turning this on, run five historical transactions through the ledger. Pick one smooth closing, one late deposit, one lender documentation request, one cancellation, and one payment-instruction change. If the system cannot distinguish those cases, it is not ready for client-facing AI.

Then review the generated drafts. They should be shorter, less certain, and more evidence-based than a generic chatbot answer. The best output is not “you are fine.” It is “here is what we have verified, here is what is still open, and here is who is reviewing the decision.”

That is the standard real estate teams should use before AI explains earnest money. The model can help clients understand the process. The ledger keeps the model from pretending it owns the outcome.

Written by

Ben Laube

AI Implementation Strategist & Real Estate Tech Expert

Ben Laube helps real estate professionals and businesses harness the power of AI to scale operations, increase productivity, and build intelligent systems. With deep expertise in AI implementation, automation, and real estate technology, Ben delivers practical strategies that drive measurable results.

View full profile