Build a Seller Net Sheet Approval Queue Before AI Talks Proceeds

AI is useful when a seller asks the question every listing team hears: "What will I walk away with?" A model can turn sale price, payoff, commission, credits, closing costs, taxes, and timing into a readable explanation in seconds. That speed is valuable, but it also creates a dangerous failure mode. If the inputs are estimates, stale, missing, or mixed with tax-sensitive assumptions, AI can make a tentative net sheet sound like a final answer.

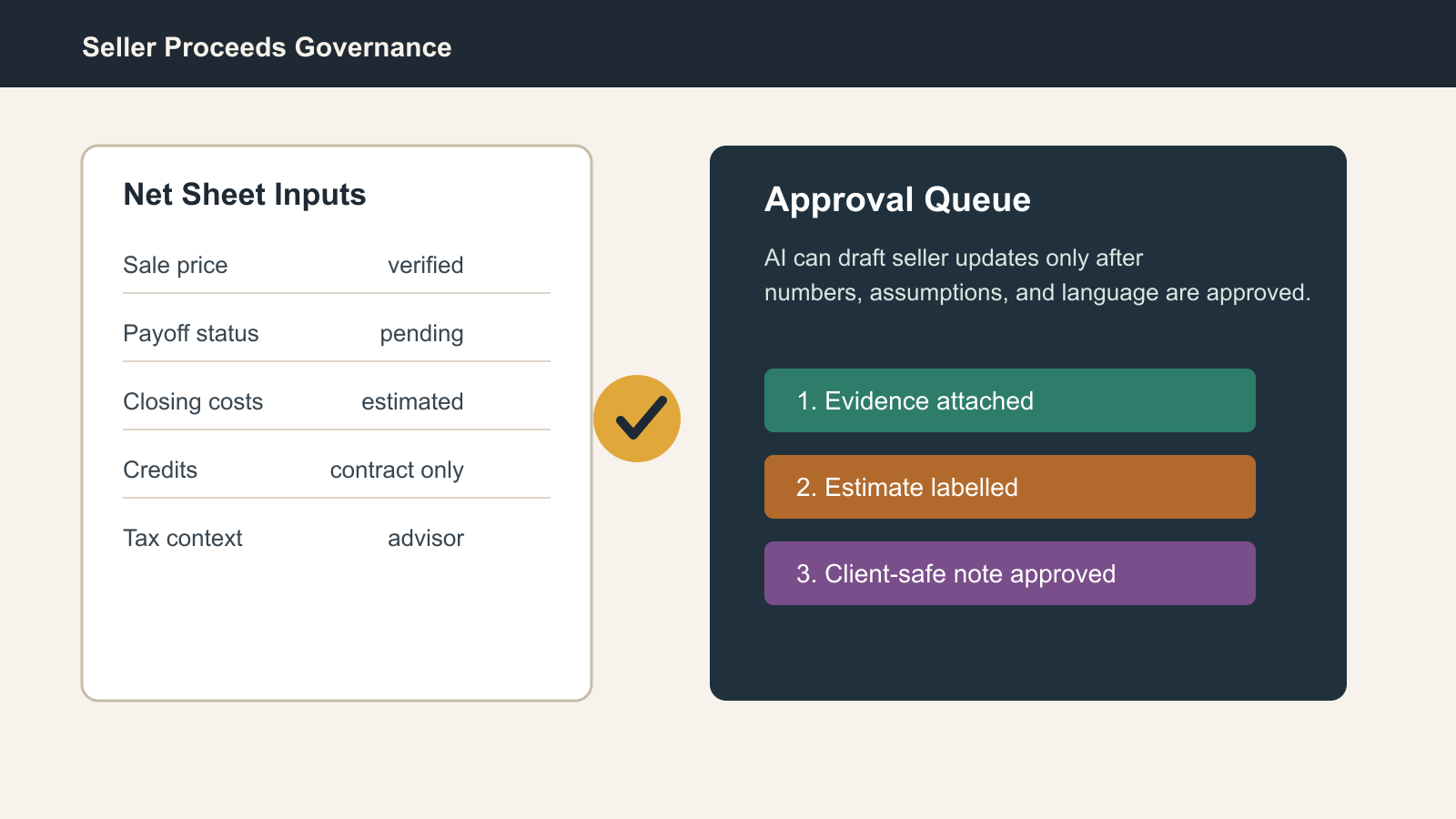

Real estate teams need a seller net sheet approval queue before AI talks proceeds.

This queue is not a replacement for the agent, settlement company, lender payoff, tax professional, or closing disclosure. It is an operating layer that decides which numbers are verified, which are estimated, which are outside the team's lane, and which client-facing words AI is allowed to use. The queue gives AI enough structure to explain the math without pretending the math is final.

The pressure to automate this work is already here. NAR's 2025 technology survey found that agents who are REALTORS are using AI-generated content alongside digital tools such as eSignature, social media, and drone photography. Seller communication is a natural next target because proceeds updates are repetitive, time-sensitive, and emotionally loaded. But a seller does not hear "draft estimate" the way a workflow system does. If an AI note says the seller should net a specific amount, the seller may treat that number as reliable.

That is why the net sheet needs an approval queue, not just a template.

The problem is not the spreadsheet

Most teams already have some version of a seller net sheet. It may live in a CRM, transaction platform, spreadsheet, title-company tool, or agent worksheet. The issue is usually not whether a calculation exists. The issue is whether each input has a source, owner, freshness date, confidence label, and approved explanation.

Start with the core rows: estimated sale price, current contract price if under agreement, mortgage payoff, any second lien or home equity line payoff, prorated property taxes, transfer taxes or local fees, title and settlement charges, recording costs, broker compensation, buyer credits, repair credits, home warranty charges, HOA or condo items, seller-paid closing costs, outstanding assessments, utility escrows if applicable, and any personal-property allocation that should stay out of the home-sale number.

Then add a status column that controls what AI may say. Use "estimate only" when the row comes from a planning assumption. Use "source attached" when the row has a document, invoice, payoff, contract clause, closing-cost estimate, or settlement draft behind it. Use "third-party pending" when the team is waiting on title, lender, HOA, attorney, accountant, or another authority. Use "client decision needed" when the number depends on seller approval. Use "do not summarize" for anything that should not be translated into client-facing advice.

That status column matters because seller proceeds are not one number. They are a stack of assumptions.

Separate proceeds math from tax interpretation

The IRS page for Publication 523 explains that the publication covers tax rules for selling or otherwise giving up ownership of a home, and the current page was last reviewed or updated on March 31, 2026. The 2025 Publication 523 itself walks through gain or loss using selling price, selling expenses, amount realized, adjusted basis, and other tax concepts. That is useful context, but it also proves why a real estate team should not let AI blur the line between proceeds math and tax advice.

A seller net sheet can estimate cash at closing. It should not casually tell the seller what will be taxable, what qualifies for exclusion, how improvements affect basis, or whether a personal circumstance changes the answer. AI can say, "This net sheet is an estimated cash-at-closing view, not tax advice." It can also say, "Tax impact depends on your basis, use, ownership history, prior exclusions, and advisor guidance." It should not convert a net sheet into a tax conclusion.

Build this into the queue with a tax-context field. The field should not ask the agent to solve the tax issue. It should identify the boundary: routine sale with no known tax discussion, seller asked tax question, investment or mixed-use property, inherited property, divorce or estate context, business use, prior rental use, short ownership period, or advisor required. Any non-routine tax-context status should block AI from giving proceeds language beyond the narrow estimate.

Make closing-cost language evidence based

The CFPB's Closing Disclosure guidance explains that the form gives final details about a mortgage loan, including loan terms, projected payments, fees, and closing costs. CFPB guidance on who pays mortgage closing charges also notes that some costs may be paid by the seller depending on the contract or state law. Those two points are enough to shape a practical rule for real estate operations: AI should not explain seller-paid costs unless the queue knows whether the row is estimated, contract-based, title-provided, or final-document based.

Use four evidence types.

The first is planning estimate. This is useful before a listing agreement, price improvement, or offer review, but the client-facing language should stay soft: "Using the current assumptions, estimated proceeds would be approximately..."

The second is contract evidence. This means the purchase agreement, addendum, concession term, repair credit, or compensation term has been attached. AI may describe what the contract says, but it should still avoid treating every downstream cost as final.

The third is third-party estimate. This may come from title, escrow, attorney, lender payoff, HOA, or a settlement worksheet. AI may cite the source and date internally, then give the seller a cleaner note: "This estimate uses the title company's May 6 worksheet and the payoff currently on file."

The fourth is final or closing-package evidence. This is the narrowest lane. AI can say the number reflects the final closing package only when the queue is tied to the correct document version and reviewer.

Without those evidence types, AI will smooth over uncertainty. With them, the model can be helpful and restrained.

Add approval roles before automation writes to the seller

NIST's AI Risk Management Framework is organized around managing AI risk across the lifecycle, and its 2026 page highlights continuing profile work for trustworthy AI. In a small real estate team, the practical translation is simple: decide who approves the system's inputs and outputs before the output reaches the client.

A seller net sheet approval queue should have at least three roles.

The preparer assembles the rows and attaches evidence. This may be the agent, transaction coordinator, listing manager, or operations assistant. The preparer is responsible for freshness: payoff requested date, title estimate date, contract version, and last seller decision.

The reviewer checks math and language boundaries. The reviewer should ask whether every material number has a status, whether any row is stale, whether client-facing notes overstate certainty, and whether tax, legal, payoff, or settlement questions need a third party.

The sender owns the relationship. The sender decides whether the seller should receive the AI-drafted explanation as-is, receive a narrower note, or get a call instead. This role matters because proceeds questions often appear at emotional moments: after a price reduction, after an offer, after an inspection credit, after a title issue, or right before closing.

AI can draft, compare versions, and detect missing fields. It should not be the final approver.

Use language bands instead of one confident answer

The queue should map each status to a language band. A planning net sheet should produce planning language. A contract-backed estimate should produce contract language. A final settlement package should produce final-document language.

Planning language: "Based on the assumptions currently in the worksheet, your estimated proceeds are approximately... This will change when payoff, title, prorations, credits, and closing costs are confirmed."

Contract language: "Using the signed contract price and currently attached seller-credit terms, the estimated proceeds range is... Payoff, title, prorations, and settlement charges still need confirmation."

Third-party estimate language: "Using the title or settlement estimate dated [date] and the payoff information currently on file, the estimated proceeds are... Please treat this as an estimate until final closing documents are issued."

Final-document language: "This reflects the closing package version reviewed on [date]. Confirm any tax or advisory questions with your tax or legal professional."

The model should choose from these bands based on queue status, not its own confidence. The queue controls certainty. AI controls readability.

The minimum viable queue

A team can build the first version in a spreadsheet, CRM custom object, or transaction board. The minimum fields are simple: deal ID, seller, property, scenario name, sale price or assumed price, payoff source and date, cost rows, credit rows, evidence links, status, tax-context boundary, reviewer, client-safe note, and send approval.

Add three automations after the manual queue works.

First, alert when a row has no evidence source. Second, flag stale rows when a payoff, title estimate, or contract version is older than the team's threshold. Third, block AI from sending seller proceeds language unless the scenario has a reviewer and a client-safe note.

Then let AI do what it is good at. It can draft a plain-English explanation, compare the current version against the prior version, summarize which rows changed, prepare questions for the settlement company, and generate an internal risk note. It can also produce a seller-friendly range instead of a single false-precision number.

The benefit is not just fewer mistakes. It is better trust. Sellers can see that the team is not hiding behind automation. They are using automation to make the math clearer while keeping the authority of the numbers visible.

Seller proceeds are too important for AI to improvise from a spreadsheet. Build the approval queue first, then let the model turn verified assumptions into useful communication.

Written by

Ben Laube

AI Implementation Strategist & Real Estate Tech Expert

Ben Laube helps real estate professionals and businesses harness the power of AI to scale operations, increase productivity, and build intelligent systems. With deep expertise in AI implementation, automation, and real estate technology, Ben delivers practical strategies that drive measurable results.

View full profile