Build a Buyer Budget Drift Desk Before AI Changes Searches

Real estate teams are starting to let AI adjust search alerts, summarize buyer intent, recommend neighborhoods, and draft "new match" messages. That creates leverage only if the buyer's budget is treated as a live operating constraint rather than a static field from the first consultation.

A buyer can drift out of range without ever saying, "my budget changed." Rates move, taxes update, insurance quotes arrive, HOA dues appear, down payment assumptions change, a lender revises the preapproval, or a buyer simply decides that the monthly payment feels different after seeing real homes. If AI keeps widening the search, rewriting alerts, or nudging the buyer toward homes based on stale affordability data, the team is automating pressure instead of service.

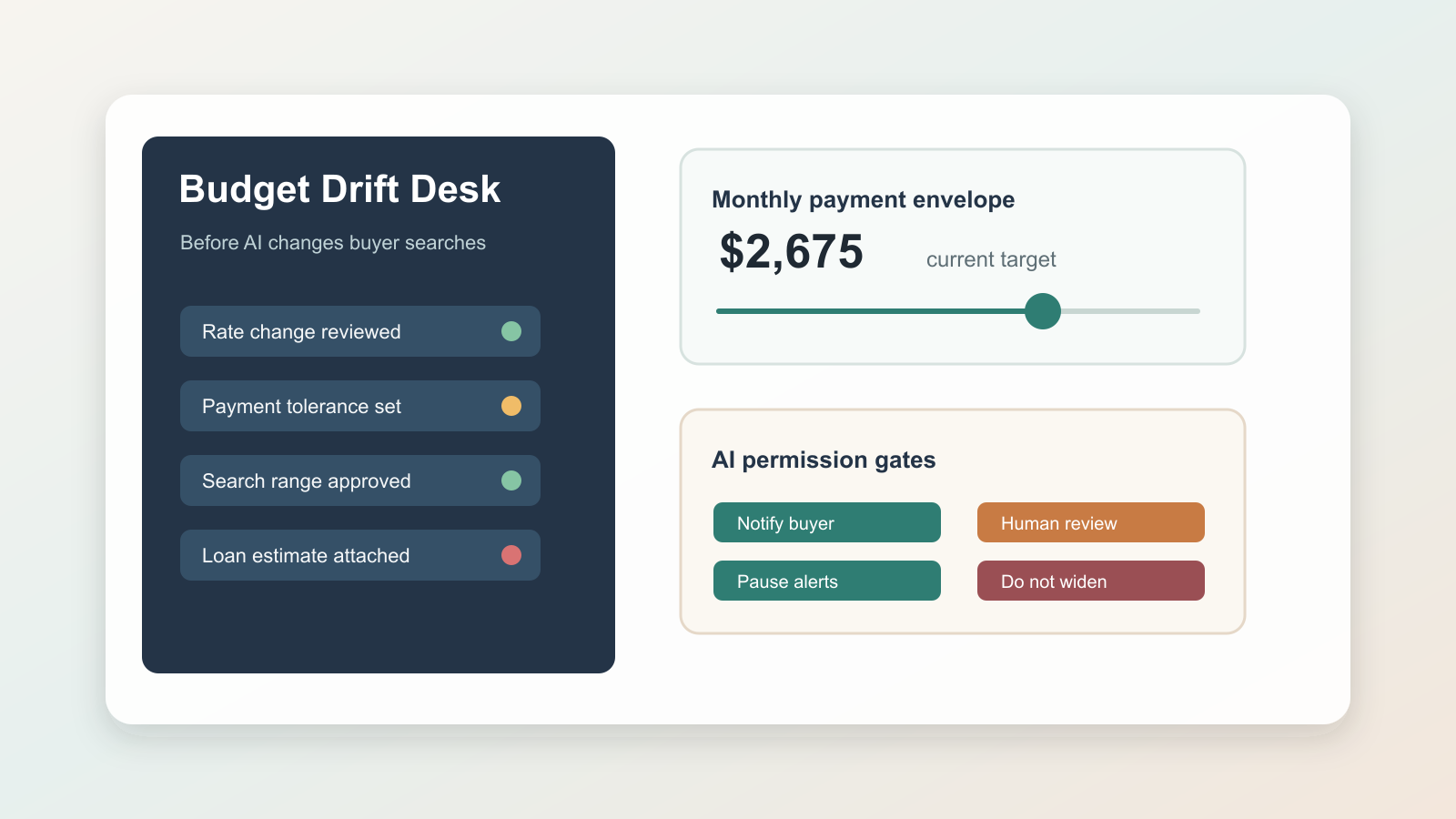

Build a buyer budget drift desk before AI changes searches. The desk is a small control surface inside the CRM that says what changed, who verified it, what AI is allowed to do next, and when the buyer must approve a new range.

The market makes budget drift normal

Budget drift is not a corner case in 2026. Freddie Mac's April 30, 2026 Primary Mortgage Market Survey put the 30-year fixed-rate mortgage average at 6.30%, up from 6.23% the prior week, while noting that purchase applications were more than 20% above the prior year as buyers reacted to modestly lower rates and more inventory. That combination matters: more buyers are active, but their payment math is still rate-sensitive.

Fannie Mae's April 2026 housing forecast shows the same need for active recalculation. It estimates the 30-year fixed-rate mortgage at 6.1% in Q1 2026, 6.3% in Q2, 6.2% in Q3, and 6.1% in Q4. Even if the annual average looks stable, the quarter-to-quarter movement can change a buyer's payment tolerance and the homes that deserve attention.

Redfin's February 2026 affordability analysis found that Americans needed $111,252 per year to afford the typical U.S. home for sale, down 4% from a year earlier, with the required income having peaked above $122,000 in June 2025. That is encouraging, but it also means affordability is moving enough that automated search logic should be recalibrated deliberately rather than improvised by prompts.

NerdWallet's 2026 Home Buyer Report adds the AI adoption pressure. It found that 48% of prospective buyers plan to use AI tools during the homebuying process, including 27% for estimating housing costs. The same report found that 40% of prospective buyers consider themselves house poor and that taxes, insurance, HOA dues, repairs, and escrow changes can make the real monthly number feel different from the simple mortgage estimate. Buyers are already asking software to help with the math. Your CRM should know when the math is official enough to change the search.

What the desk tracks

The budget drift desk is not a lender portal and it should not pretend to underwrite a buyer. It is an operational record that keeps the team from letting AI act on stale assumptions.

Start with the buyer's approved payment envelope. Store the maximum comfortable monthly payment, not only the top purchase price. Capture the components that make the number usable: principal and interest assumption, estimated taxes, insurance range, HOA ceiling, mortgage insurance expectation, cash-to-close target, and post-closing reserve preference. A buyer who can technically qualify at one number may still only want to live at another.

Next, store the source of authority. A lender conversation, updated preapproval, Loan Estimate, buyer-written confirmation, or agent note should not all carry the same weight. The CFPB explains that lenders are required to provide a Loan Estimate after receiving six pieces of information, and that the estimate shows expected loan terms if the buyer moves forward. That is a stronger trigger than a casual text about hoping rates improve.

Then track the drift event. Did a rate quote move? Did the buyer add a required bedroom? Did HOA dues make a condo segment unattractive? Did insurance or property taxes change the payment? Did seller credits, down payment assistance, or a builder buy-down create room that expires? The desk should name the event, timestamp it, attach the evidence, and mark whether it raises, lowers, freezes, or narrows the search range.

Finally, define the AI permission state. AI may be allowed to notify the buyer that a saved search needs review. It may be allowed to pause alerts above the approved payment envelope. It may be allowed to draft a message explaining tradeoffs. It should not automatically widen the price range, remove must-have constraints, suggest riskier financing, or pressure a buyer to chase homes that no longer fit.

The workflow

The desk needs four states.

First is current. The buyer has a verified budget record, the source is fresh, and AI can use the approved range for alerts, summaries, and listing recommendations.

Second is watch. A signal changed, but not enough to change behavior yet. For example, rates moved slightly, new listings are appearing in a target neighborhood, or the buyer asked about a higher range without confirming comfort. AI can flag the account for review and prepare comparison notes, but it should keep the current search rules.

Third is review required. The change could materially alter the buyer's monthly payment, cash-to-close, or tradeoffs. AI can prepare the brief: old range, new possible range, source, payment delta, affected searches, and pending questions. A human should decide whether to call the buyer, lender, or both.

Fourth is locked. The budget record is expired, contradicted, missing lender evidence, or explicitly rejected by the buyer. AI should stop changing search alerts and stop drafting affordability advice until the desk is restored to current.

This state model is useful because it converts affordability uncertainty into routing. The agent does not have to read every note. The CRM shows which buyers can receive automated search help and which ones require human review.

What AI can do safely

AI is valuable around the desk when it is constrained to evidence handling and communication support.

It can summarize the last verified budget, list open questions, identify listings that are now outside the payment envelope, detect when an HOA fee pushes a property above tolerance, and draft a plain-English explanation of why the search range should be reviewed. It can compare buyer preferences against the approved range and show which tradeoffs preserve the payment goal.

It can also produce a weekly budget drift queue for the team: buyers with stale preapprovals, buyers whose saved searches include homes above the approved envelope, buyers with rate-sensitive budgets, and buyers whose recent clicks suggest a higher or lower range than the one on file.

The boundary is important. AI should not decide that a buyer can afford more because a calculator says so. It should not interpret lender screenshots without review. It should not assume a buyer wants to trade reserves for purchase price. It should not convert aspirational browsing into a new search range. The desk turns AI into an assistant for budget governance, not a hidden sales manager.

Fields to add this week

You do not need a large rebuild. Add these fields to the buyer record or a related budget table:

- approved monthly payment envelope

- approved price range

- cash-to-close target

- reserve preference

- rate assumption and expiration date

- tax, insurance, HOA, and mortgage insurance assumptions

- authority source

- source attachment or link

- last verified date

- next review date

- drift event type

- AI permission state

- human owner

- buyer approval status

Then add one automation rule: if the budget source is older than the team's policy window, or a search result exceeds the payment envelope by more than the approved tolerance, set the account to review required before AI changes alerts.

The implementation rule

The point is not to make the CRM calculate every mortgage scenario perfectly. The point is to make the CRM honest about what is verified, what changed, and who is allowed to act.

AI search automation works when the buyer's budget is treated as a governed object. Without that, the system will eventually do one of two bad things: keep sending homes the buyer cannot comfortably carry, or overcorrect and hide viable options because a stale assumption was never reviewed.

A budget drift desk gives the team a practical middle path. It keeps buyer searches responsive to the 2026 market, gives agents a clear review queue, and lets AI help with the work that actually needs speed: spotting changes, preparing briefs, and keeping messages aligned with verified affordability.

Written by

Ben Laube

AI Implementation Strategist & Real Estate Tech Expert

Ben Laube helps real estate professionals and businesses harness the power of AI to scale operations, increase productivity, and build intelligent systems. With deep expertise in AI implementation, automation, and real estate technology, Ben delivers practical strategies that drive measurable results.

View full profile