Build an Insurance Claim Repair Proof Desk Before AI Summarizes Damage

AI can summarize storm damage faster than a team can sort photos, invoices, adjuster notes, contractor bids, lender conditions, and client texts. That speed is useful only if the underlying claim file is organized enough for the system to know what is verified, what is still alleged, what belongs to the insurance carrier, and what should never become client-facing advice.

That is the operational gap many real estate teams are about to feel. Agents are already using AI and digital tools in daily work. NAR reported in its 2025 Technology Survey release that 46% of agents used AI-generated content and that client response to technology in the buying and selling process was strongly positive. A newer NAR/RPR report from February 12, 2026 described AI as part of day-to-day workflows for many agents, but also said accuracy of outputs was the top concern for 63% of surveyed agents. In other words, teams are not waiting for perfect governance before using AI. They need narrower operating rooms where AI can help without pretending to be an adjuster, contractor, lender, attorney, or disclosure authority.

Post-loss repair documentation is one of those rooms. A claim file touches real money, property condition, financing, closing timing, future insurability, client trust, and sometimes government assistance. If AI is allowed to summarize the file from scattered artifacts, it may blur temporary repairs with permanent repairs, confuse an estimate with an approved scope, treat a settlement letter as final when a supplement is pending, or draft confident language before the client has documentation to support it. The fix is not a longer prompt. It is an insurance claim repair proof desk: a structured CRM workspace that separates evidence capture, authority checks, and approved communication.

Why this desk matters now

The documentation burden is not theoretical. The California Department of Insurance Residential Property Claims Guide, revised February 28, 2025, tells homeowners to protect property after a loss, save receipts for materials, avoid extensive permanent repairs until the adjuster has assessed the damage, keep a log of calls and correspondence, and understand that a proof-of-loss form may be required. The guide also explains that the adjuster's scope of loss should capture damage degree, material and workmanship quality, and measurements needed for estimating.

Texas Department of Insurance guidance for disaster claims gives similar operational signals: temporary repairs are generally acceptable, but owners should take pictures before doing work. It also notes that additional claim payments can depend on proof that repair work is being done. FEMA's applicant guidance adds another layer. If FEMA needs more information, it may request an insurance settlement, a denial, receipts for disaster costs, repair estimates, or other documents showing why assistance is still needed. These are not just attachments. They are timeline-sensitive proof objects.

The risk grows when contractors enter the file. The FTC warns consumers to be careful with home improvement scams, especially pressure tactics, upfront cash demands, blank spaces in contracts, contractor-arranged financing, and work that is incomplete or shoddy. Its advice includes checking license and insurance, getting multiple written estimates, making sure written contracts include key details, and holding final payment until work is done and satisfactory. An AI assistant that drafts updates from a contractor text without checking license proof, contract status, estimate scope, payment status, and completion evidence can turn an operational shortcut into a client service risk.

NIST's AI Risk Management Framework is useful here because it shifts the question from "Can the model write this?" to "Can the organization map, measure, manage, and govern the risk of using the model in this workflow?" NIST's AI RMF page, updated with new 2026 activity around trustworthy AI profiles, frames AI risk management as an organizational practice, not a one-time model choice. For a brokerage, property management team, investor operator, or home-service-heavy advisory team, the practical translation is simple: do not let AI summarize claims until the claim data model says what each document is, who verified it, what decision it can support, and what language is approved.

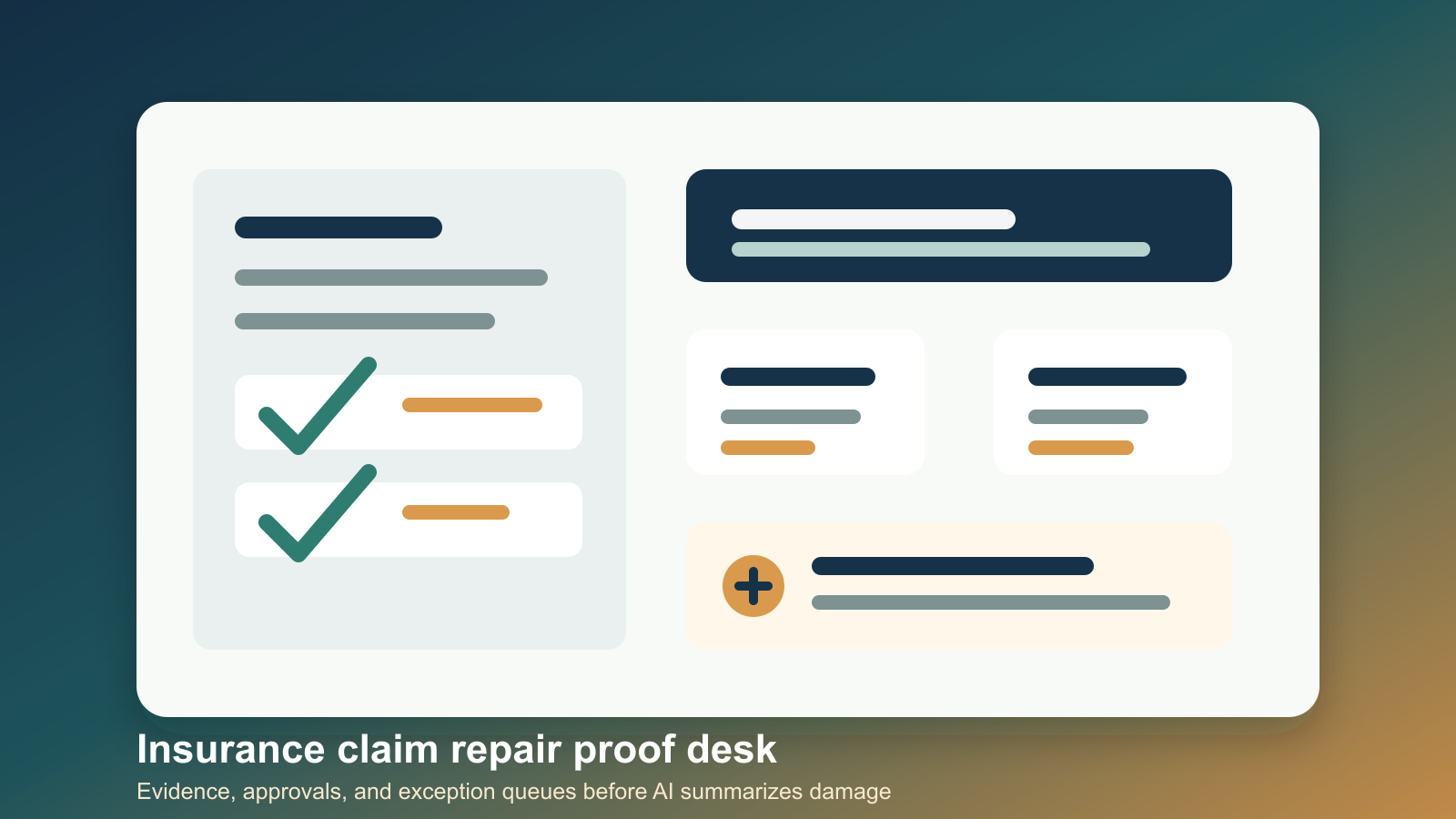

The desk is a source system, not a folder

A folder full of PDFs is not enough. The proof desk should be a CRM-backed source system with a repeatable schema. Each claim-related item needs a type, owner, date, status, source, verification state, and allowed use.

Start with the claim header. Capture the property, parties, date of loss, claim number, carrier, adjuster, policy contact, mortgage or lender contact when relevant, and internal owner. Record whether the team is helping the client organize documents, coordinating post-close service, preparing a listing file, managing an investor repair project, or supporting a transaction already under contract. That role matters because it controls what the team can say.

Then define the proof objects. A strong desk distinguishes damage photos, mitigation receipts, contractor estimates, signed contracts, change orders, permits, inspections, carrier scopes, settlement letters, denial letters, supplement requests, paid invoices, completion photos, lien waivers, lender draw conditions, and client approvals. These should not be dumped into one "documents" field. They should be structured enough for a workflow to ask, "Do we have a dated photo before repair? Do we have the estimate and the approved scope? Do we have proof that the temporary repair was done to prevent further damage? Do we have completion proof before the final client update goes out?"

Next, attach authority labels. Carrier documents can support what the insurer has stated, but they do not prove code compliance. Contractor bids can support scope and pricing conversations, but they are not settlement approvals. Photos can support visible condition, but they are not engineering conclusions. FEMA letters can show requested documents, but they are not a substitute for insurance coverage review. These labels keep AI from overusing the wrong evidence.

What AI may do inside the desk

Once the proof desk exists, AI can be useful in narrow ways. It can classify uploaded documents, extract dates and claim numbers, draft internal checklists, identify missing artifacts, compare contractor estimates against the carrier scope, flag blank contract fields, summarize next actions for staff, and prepare non-advisory client status notes for human review. It can also generate exception queues: missing pre-repair photos, no receipt for emergency materials, final payment requested before completion proof, contractor insurance not verified, settlement letter absent, permit status unknown, or lender draw package incomplete.

Those are high-leverage tasks because they improve file quality before anyone writes public-facing or client-facing language. The desk should treat AI output as work product that must be reviewed, not as final authority. A clean rule is that AI can summarize the file state, but it cannot interpret coverage, guarantee reimbursement, decide whether a claim should be filed, make legal disclosure conclusions, approve contractor payment, or represent that repairs satisfy code or lender requirements.

The system should also separate internal notes from approved language. Internal notes can be blunt: "Carrier settlement letter missing" or "contractor invoice does not match estimate line items." Client language needs review and context: "We are still missing the carrier settlement letter and final paid invoice, so the repair packet is not ready for closing/lender/disclosure review." That difference is where many AI workflows fail. They turn internal uncertainty into polished confidence.

Minimum viable workflow

The first version can be lightweight. Build one CRM object called Insurance Claim Repair Proof Desk and relate it to contacts, property records, transactions, and service tickets. Add the claim header fields, proof-object table, authority labels, and exception statuses. Require every proof object to have a source URL or file, received date, document date, verifier, and allowed-use tag.

Use five statuses: intake, awaiting proof, under review, approved for communication, and closed. Keep a separate exception list for missing or conflicting evidence. Add one human approval step before any client-facing AI summary can be sent. If the workflow involves a transaction, make sure transaction leadership or the designated compliance reviewer can see the desk before disclosure-sensitive language leaves the system.

The most important automation is not the summary. It is the missing-proof detector. Before AI drafts a status note, it should check for the evidence required by the situation. A temporary repair update should require photos, date of damage, receipt or invoice, and whether an adjuster inspection is complete. A contractor status update should require license/insurance verification status, written estimate or contract, payment terms, and completion evidence. A FEMA assistance update should require the FEMA request letter, insurance settlement or denial status, and receipts or estimates being supplied. A listing or transaction update should require an internal review flag because claims and repairs may affect disclosure, lender, appraisal, and buyer questions.

What to measure

A proof desk should produce operational metrics, not just cleaner notes. Track average time from claim intake to complete proof packet, percentage of files missing pre-repair photos, percentage of contractor packets missing license or insurance evidence, number of AI summaries blocked by missing authority, number of client updates revised by human reviewers, and number of reopened exceptions after a file was marked ready.

Those metrics matter because they show whether AI is reducing work or just hiding mess behind better prose. If the exception queue grows, the team has a process problem. If summaries are often rewritten, the approved-language library is weak. If documents are present but misclassified, the upload intake needs better categories. If final payment questions appear before completion proof, the desk is catching real operational risk.

The implementation principle

The principle is straightforward: let AI accelerate claim repair coordination only after the evidence model is stronger than the writing model. Insurance and repair files are too consequential for loose summaries. The team needs dated proof, source authority, missing-document checks, and human approval gates before automation touches client-facing language.

A well-built insurance claim repair proof desk does not make the brokerage an insurance expert. It makes the operational record clearer. It helps staff know what is missing, gives reviewers a consistent evidence map, and gives AI a bounded role it can perform well. That is the kind of automation that actually improves service: faster coordination, less unsupported language, and a cleaner handoff when the file moves from damage event to repair proof to transaction decision.

Written by

Ben Laube

AI Implementation Strategist & Real Estate Tech Expert

Ben Laube helps real estate professionals and businesses harness the power of AI to scale operations, increase productivity, and build intelligent systems. With deep expertise in AI implementation, automation, and real estate technology, Ben delivers practical strategies that drive measurable results.

View full profile